Disclaimer: I’m not an investment advisor. Nothing in this article should be taken as investment advice. This article is for informational and educational purposes only and should not be considered financial or investment advice. Always do your own research and consult a financial advisor before making any investment decisions. I currently hold shares in $ESAF.

Syntholene: Fingerprints of 100 bagger

12-18 month Target: $4 to $10 CAD

3 year Price Target: $8 to $25 CAD

5 Year Price Target: $25 to $50+ CAD

Ticker: $ESAF.V | Price: 0.56 CAD | Fully Diluted Shares Outstanding: 77.69M | Market Cap: ~ 50M CAD | Net Cash: ~ $4M | Insider Ownership: 52.6% + Shell holds ~ 8%

Overview

Syntholene is a development stage company actively commercializing a counter-positioned electro-synthetic sustainable aviation fuel (e-SAF) production pathway targeting 70% lower cost than the nearest competitor. Sytholene’s cost advantage stems from their proprietary integration with geothermal plants that utilizes excess/waste heat to offset electricity costs. Sytholene’s long term plans also involve producing synthetic fuels for marine use, as well as, long-haul trucking. Long-term they also envision integration into nuclear facilities to utilize those facilities’ excess heat. Although syntholene’s integrations are unique and proprietary, their processes use existing proven technologies. The Company's mission is to deliver the world's first truly high-performance, low-cost, and carbon-neutral synthetic fuel at an industrial scale. Within the next 5 years, the company targets production costs below fossil fuel derived aviation fuel.

In December of 2025, Syntholene completed a reverse takeover to become publicly listed on the TSX-V and subsequently, also listed on the OTCQB and Frankfurt Stock Exchange.

To fully understand Syntholene’s value proposition, we will first examine the highly regulated and emerging industry of e-SAF. We will then turn to a brief discussion of thermodynamics and green hydrogen technologies, as it is an intermediate feedstock. Then we will discuss Syntholene’s current operations, management, risk, and valuation.

E-SAF, SAF, and EU Regulations - Creating Industry Demand

Electro-synthetic sustainable aviation fuel (e-SAF) is a different commoditized product than sustainable aviation fuel (SAF) and has its own separate emerging market. Currently, e-SAF fetches a premium price compared to bio-based SAF (~$7.12/L; ~$2.53/L).

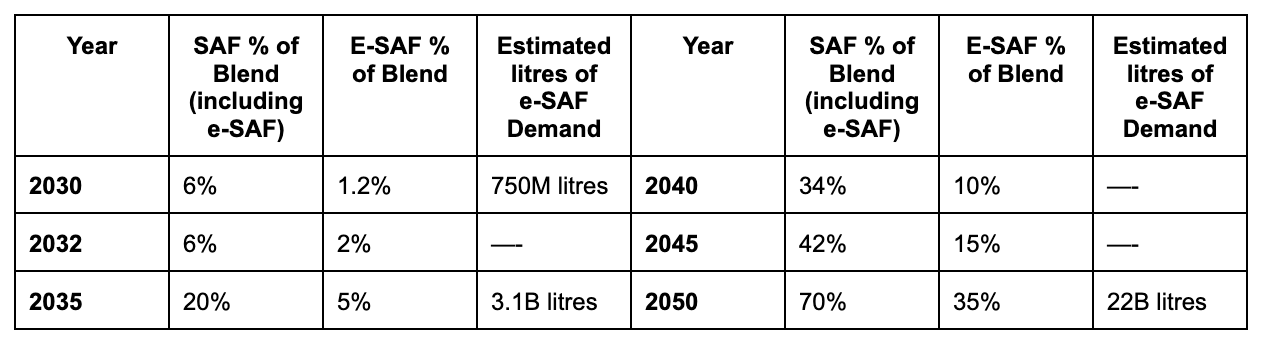

Demand for e-SAF is being driven by strict mandates in the European Union, United Kingdom, Japan, and British Columbia. ReFuelEU Aviation Regulation has a specific sub-mandate requiring airlines to use e-SAF starting in 2030. The table below sets out specific blend ratios for e-SAF.

The estimated demand for e-SAF from 2030 to 2035 has a CAGR of 32.8%. From 2035 to 2050, we see a CAGR of 13.96%. The Overall period CAGR from 2030 to 2050 is 18.4%.

Limited data exists on the supply side of e-SAF. However, Syntholene has internally modelled the supply and demand for e-SAF. Their graph illustrating the shortfall is set out below.

Industry CAP Ex Driver - Restricted Feedstock and Production

For these next two sections, it is important to understand that fossil fuels, synthetic fuels and sustainable aviation fuels are all hydrocarbons. All hydrocarbons are chains or structures of carbon atoms with hydrogen attached, for example kerosene (aviation fuel):

Thus, to produce synthetic kerosene and synthetic fuels, companies need to source carbon and hydrogen.

The EU also regulates how e-SAF can be produced by restricting potential feedstocks to renewable electricity/green hydrogen and captured carbon, explicitly excluding biological/biomass (crop/waste) sources. These regulations apply to e-SAF production regardless of geographic location. Currently, the most costly and highest demand input for e-SAF is renewable electricity to produce green hydrogen, a reaction intermediate.

The EU has implemented policies to ensure that renewable electricity used to produce e-SAF does not simply take existing energy but prompts the development of new renewable energy infrastructure. The regulations delineate between direct connections or grid connections for e-SAF production.

For operations with direct connections between a renewable electricity source and e-SAF production, the following rules apply: 1) there must be a direct connection between the facilities or they must be part of the same installation; 2) the renewable electricity must come into operation not earlier than 36 months before the installation of the e-SAF production facility; 3) the renewable electricity source cannot be connected to the grid or must use smart meters to show that no electricity is being diverted from the grid.

For operations using renewable electricity from the grid, the following laws apply:

For the grid to qualify, it must have renewable electricity as 90% of total electricity the prior year (Norway; Iceland; and northern zones in Sweden). Limits: The number of full-load operating hours cannot exceed the exact proportion of renewable electricity in that bidding zone multiplied by 8,760 (the number of hours in a year). Example: If the zone was 94% renewable in the previous calendar year, the producer can operate for a maximum of 8,234 hours that year (0.94 × 8,760).

Alternatively, a grid can qualify as renewable electricity if the emission intensity is lower than 18 gCO2eq/MJ (Sweden; Norway; Iceland; Finland; France; Switzerland; Austria). To qualify for producing e-SAF, there must also be a signed Power Purchase Agreement with an existing renewable energy operator; the electrolyser must be part of the same local grid as the renewable energy operator; and, there must be a temporal connection between electricity production and e-SAF production. Currently, the renewable electricity must have been generated in the same month as the e-SAF is produced. Starting January 1, 2030, the renewable electricity will have to be produced within the same hour as the e-SAF production.

Although there are exceptions that allow e-SAF producers to integrate into the grid, the reality is that there is not enough extra electricity to create any kind of meaningful production. Outside of France, there is nearly no excess electricity in Europe that’s not already spoken for. This means e-SAF producers essentially have to partner or finance new renewable energy installations. Current industry practice is for companies to build their own solar and wind farms adjacent to their e-SAF production (see for example: European Energy; German efuel One GmbH; Grafroce; HIF Global; Prometheus Fuels; Twelve; Infinium; LanzaJet; Skynrg).

Industry Op Cost Driver: Green Hydrogen

There are two commercial pathways that dominate the production of e-SAF: Fischer-Tropsche; and, Methanol-to-Jet. These pathways are commercially proven and are ‘catalog’ items. The economic choke point for each pathway is the marginal cost of green hydrogen.There are global initiatives to develop green hydrogen technologies to produce sub $2/kg hydrogen; however, the lowest verified unsubsidized production costs remain firmly anchored between $2.50/kg and $3.50/kg. Syntholene’s cost estimates for green hydrogen production target costs below $1.50/kg and, long term, <$1.00/kg. Now, let me explain how this is possible.

To produce green hydrogen, the hydrogen atoms in water need to be split from oxygen. Currently, there are three green hydrogen technologies competing for dominance: Proton Exchange Membrane (PEM) technology; Alkaline Water Electrolysis (AWE); and Solid Oxide Electrolyzer Cells (SOEC). The majority of the operating cost of each technology is electricity.

Syntholene has entered an agreement to use Dynelectro’s SOECs. Dynelectro claims to have the world’s most efficient SOEC reporting 95% electrical efficiency. Compare this to the average efficiency of AWE at 63%-70% and PEM efficiency at 56%-60%. The efficiency gains within SOEC technologies come down to some fundamental principles of thermodynamics and using heated water to do the heavy lifting instead of relying entirely on electricity.

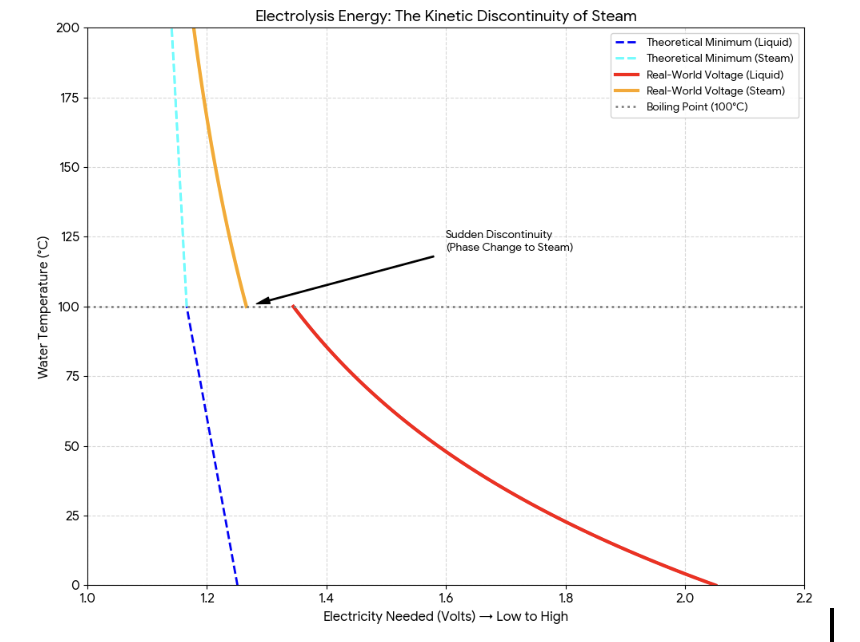

So why do SOECs have increased efficiency? Essentially, the amount of electricity required to break water apart is dependent on the temperature of water and its state (liquid or steam). As water is heated, the molecules move faster and faster, increasing kinetic energy, and its hydrogen bonds stretch and weaken, increasing potential energy. During the transition to steam, the heat energy stops increasing the molecules' speed (kinetic energy) and instead focuses on breaking their bonds (increasing potential energy), allowing them to expand into a high-energy gas. Effectively, the heat performs the preliminary work of destabilizing water’s molecular structure, allowing the electrolyzer to achieve the same chemical result with a lower voltage and less electrical current. Below, you will find a graph I created to help illustrate this relationship:

When water transitions from liquid to steam, the efficiency of electrolysis experiences a sudden, dramatic leap because the physical "friction" of the system practically vanishes. This efficiency gain is not available with AWE or PEM as both use water for their respective processes. In liquid water, ions must fight through a dense, viscous medium, and the newly split hydrogen and oxygen form insulating gas bubbles on the electrodes that choke off the electrical current. Once water vaporizes into steam, these physical barriers disappear instantly. The mass transport of molecules becomes nearly frictionless and the bubble problem is eliminated, dropping the real-world electrical resistance (overpotential) and sharply reducing the total electricity required to force the reaction. SOECs are specifically engineered to weaponize this steam-phase efficiency by operating at blistering temperatures.

Note: If electricity is used to heat water for SOECs, it yields no significant electricity savings for e-SAF production; according to the laws of thermodynamics, you are simply shifting the energy load from electrolysis to heating rather than reducing the total power required.

Minimizing Electricity: Syntholene’s Innovative Integration

Syntholene has cleverly innovated a method of vertical integration with geothermal plants that captures excess/waste heat to pre-heat water feedstock before their SOECs. Academic literature indicates that there is a potential 20-30% reduction in overall electricity costs if thermal inputs are available (Buttler & Spliethoff, 2018). I call the innovation clever as it involves existing proven technologies being utilized in a novel integration that qualifies for patent protection. Together, this means low technological risk, high commercial value and a defensible moat. So how do they do it?

Geothermal Plants essentially use pressure and heat from geothermal brines to spin turbines. Turbines are around 70%-80% efficient. But overall, geothermal plants are relatively inefficient only capturing approximately ~20% of geothermal heat before it is reinjected into the earth. Some of the inefficiency is required as geothermal brine cannot be reinjected back into the earth cold needing to remain above approximately 120oC.

Syntholene plans to integrate into geothermal plants diverting a relatively small amount of brine ahead of the turbines that generate electricity. Since electrolysers require purified water and geothermal brine has many contaminants, the geothermal brine can’t be piped directly into the electrolyzer. Instead, the geothermal brine is piped into a proprietary heat exchanger skid.This heat exchanger skid keeps the geothermal brine in a closed loop. On the other side of the exchanger is a separate loop of purified water. By co-locating these pipes and using existing heat transfer technologies, the geothermal heat causes the purified water in the second loop to boil and turn into industrial-grade steam. The brine is then returned to the geothermal plant. Sytholene also plans to advance heat capture technologies to utilize any and all waste heat available. As commented by the CEO, “my chief engineer is stingy about his BTUs. We must use every BTU judiciously and so we have another family of patents in that category as well.”

Syntholene’s preliminary Engineering estimates indicate that using Dynelectro’s electrolyzers will allow them to produce green hydrogen for less than $1.50/kg. At scale, this process should yield green hydrogen for less than $1/ kg with the theoretical limits around <$0.65/kg in reach.

Syntholene: Status, Plan and Commercial Pathway

Currently, Sytholene does not have any commercial operations. In 2026, Syntholene plans to build a demonstration facility at the Husivik Power Station in Iceland. Permits have been issued and component assembly is underway. Papadakis Engineering has been selected as Syntholene’s development and integration partner for their geothermal heat exchanger skid. The demonstration facility will provide real world data for optimizing their processes, test thermal integration, load & mass balances, verify scalability and generate samples for potential off-take agreements.

Their plan is to leverage the niche integration, outlined above, to become one of the world’s lowest cost producers of green hydrogen and e-SAF. They have yet to decide on the specific commercial pathway for e-SAF production; however, they have indicated that both methanol-to-Jet and Fischer-Trope pathways are potential options. Both pathways are proven commercial processes that can be purchased from existing manufacturers as part of their ‘catalogue’.

Assuming success at the demonstration facility, their first commercial module is expected to be online by late 2028/early 2029. Capex for each module is estimated in the range of $200M to $250M. Each module is designed to produce 20,000 tonnes/year (25M liters/year) from 20MW of power. Syntholene estimates that early op costs will be $1.24/litre of e-SAF with long-term commercial targets around $0.64/litre. Currently, e-SAF sells for about $7.16 / litre with average competitor op costs estimated around $6.25/litre. This means that Syntholene potentially has a margin of $5.92/litre or more depending on e-SAF prices.

At the Husavik location, there is currently 45MW of local surplus with 150+ MW of expansion initiatives underway. Syntholene hopes that this initial site should be able to accommodate expansion of 4 more commercial modules into the early 2030s with potential annual revenues over $500M. In terms of the future, CEO, Dan Sutton, has also mentioned potential operations spanning into the USA, Canada, and other parts of Europe.

Management

Syntholene Energy Corp. is led by a highly specialized management team combining deep expertise in first-of-a-kind infrastructure deployment, heavy-industry capital markets, and advanced thermal engineering.

The operational execution is spearheaded by CEO Dan Sutton who brings 15 years of experience in sustainable infrastructure having previously founded and scaled Tantalus Labs to 150 employees and $20 million in annual revenue while executing construction the highly energy-efficient SUNLAB facility that 90% more energy efficiency than traditional indoor cannabis facilities. Tanatalus also achieved the highest revenue per employee in the cannabis industry, in addition to, top 3 performing SKUS in every major provincial market. Unfortunately, Tantalus Labs did fall victim to the Canadian government implementing an unforeseeable large tax on topline revenue resulting in their bankruptcy. However, after talking with Mr. Sutton, I do not believe Syntholene will meet this end; rather, it is part of his redemption story.The company's financial and corporate structuring is driven by Chief Development Officer Canon Bryan, a veteran company builder who has founded multiple multi-billion-dollar entities, including Uranium Energy Corp and Terrestrial Energy, where he successfully orchestrated over $1.5 billion in fundraising. The core technological foundation rests with Chief Engineer John Kutsch, a 30-year veteran of advanced systems design who previously served as the lead designer for Terrestrial Energy's Integral Molten Salt Reactor (IMSR) and holds the proprietary geothermal patents driving Syntholene’s synthetic fuel process.

Complementing the founders are key strategic technical and financial hires who perfectly align with the company's commercialization bottlenecks. Head Engineer Jack Williams, a Cambridge-educated specialist in high-temperature reactors, previously worked alongside Shell to deliver synthetic kerosene for KLM airlines, providing direct experience with the exact drop-in fuel profile Syntholene is developing. Financial discipline and public reporting are overseen by CFO Grant Tanaka, who leverages over 15 years of mine finance and capital allocation experience from major producers like Teck Resources and New Gold.

Crucially, the board of directors provides immense commercial validation, highlighted by the appointment of Steve Oldham. As the former CEO of Carbon Engineering, Oldham scaled the pioneering Direct Air Capture (DAC) company and orchestrated its $1.6 billion acquisition by Occidental Petroleum in 2023, granting Syntholene unparalleled strategic guidance regarding carbon feedstock networks and 45Q tax credit monetization. The board is rounded out by Anna Pagliaro, a senior commercial risk executive from Vizsla Silver, ensuring rigorous governance and contract structuring as the company scales its international infrastructure operations.

Competitive Position Profile

Counter-Positioned Production Model - Vertical Integration reducing Cap ex

Syntholene has a business model that is unique to both e-SAF and green hydrogen production as they can vertically integrate into existing geothermal operations. Capturing geothermal heat they are able to pre-heat the water entering the electrolyzer thereby lowering electricity needs. Avoiding having to build an entire integrated wind, solar, and battery storage facility greatly reduces op ex in the magnitude of $100s of Millions. Vertical Integration also creates ‘sticky’ relationships with their electricity and geothermal providers preventing supply side competition. Industry: As per the EU regulations, e-SAF must be produced from renewable energy. Current models rely on building their own renewable energy through solar and wind (see European Energy; German efuel One GmbH; Grafroce; HIF Global; Prometheus Fuels; Twelve; Infinium; LanzaJet; Skynrg). There is an emerging reliance on non-traditional electricity sources - for example Equilibrion and Twelve plan to use nuclear for heat and electricity. Importantly, this puts the industry in direct competition with AI data centres for supply side electricity production and equipment. This is a massive barrier to entry for any competitor.

Low Operating Costs

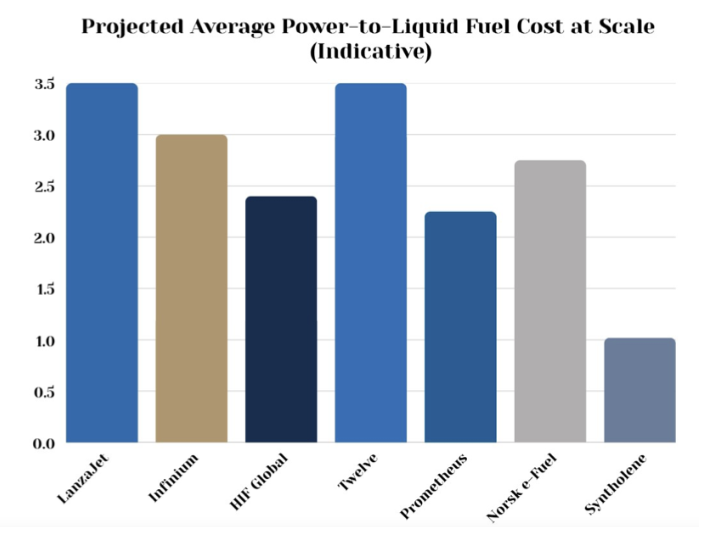

Syntholene: Syntholene’s preliminary operating costs are estimated to start at $1.24 USD per litre of e-SAF. They have also stated that their goal is and, at scale they will, produce e-SAF for less than fossil fuels. Industry: Environmental and market reports, such as those from the Clean Air Task Force, currently place synthetic e-fuels production cost in the $2.50 to $4.50 USD per litre range. Organizations like CENA Hessen have cited average production costs around €7,700 per tonne, which translates to roughly €6.16 per litre. Below, is a chart outlining op costs for comparable producers:

Distribution and Logistical Efficiency

Húsavík, where they are constructing the demonstration facility, is a coastal town that actually has its own commercial port (the Port of Húsavík). Assuming the production facility is located near the local geothermal power stations, the drive to the port would be incredibly short (likely less than 20–30 kilometers). Once production reaches 25M litres per day, syntholene would need to utilize, on average, only 2 transport truck loads per day to the Port. The close proximity to the port dramatically reduces transport and distribution costs.

Patent Protection and Intellectual Property

Syntholene’s competitive moat is protected by patents related to integrating existing technologies into geothermal plants. It also holds patents related to reactor designs. Syntholene’s patents should provide a level of protection from competition for geothermal assets (ie. suppliers)

Modular & Repeatable Technology

Sytholene is planning to deploy 20,000 tonne/annum modules that will be matched to 20MW of electricity. They hope to support 5 modules at each location. This business model allows for a scaled build out reducing the initial capital requirements and early generation of revenue to off-set capital needs and open the door to non-dilutive forms of financing. Once operating, modules also provide a safety net where maintenance on one module doesn’t necessitate shutting down the entire system.

First Mover & Early Mover Advantage

Globally, Syntholene is the first company to propose and hold the patent for vertically integrating e-SAF production into geothermal plants. Their demonstration facility will be the first of its kind. With respect to the e-SAF industry, there are currently no dominant incumbents that can scale to meet regulation driven demand. This is an emerging industry plagued with inefficiencies and high-cost producers. Syntholene will benefit from being an early entrant in terms of capital investments, potential grants, and securing off-takes.

Locking up Favourable Resources

After determining that the optimal source for pre-heating water was geothermal, Syntholene selected Iceland as their optimal geographic location. This selection is supported by Iceland’s abundant, shallow geothermal resources, skilled workforce, and proximity to major European Airports. Geothermal accounts for 30% of Iceland’s total electricity. Further, over 90% of all homes and buildings in Iceland are heated directly by geothermal district heating networks, rather than by electricity. The presence of existing large scale geothermal infrastructure gives Syntholene an advantage for expanding while maintaining a consolidated business; thereby avoiding logistical expenses. Further, by building a world first of a kind facility in Iceland, should generate local interest with potential suppliers, which should help with expansion.

Aluminum company of America is an example of a company that obtained a distinct cost advantage independent of scale due to proprietary access to favourable location. The proximity to hydroelectric power allowed Alcoa to produce aluminum at lower cost than competitors who relied on more expensive sources of energy. Alcoa had effectively cornered the market for access to some of the est sources of hydroelectric power in the US.

Lastly, Iceland is well situated for access to European markets. This will provide benefit with shipping and compliance with the regulations regarding sourcing for e-SAF for use in Europe.

Unlimited Growth Runway

Syntholene has a long growth runway in Iceland, the United States, and globally anywhere geothermal facilities exist. They do not need to buy large assets and drill wells like traditional fossil fuels. The limiting constraint on expansion will be capital and financing a sustainable growth rate.

Unlimited Fuel, Forever - Energy Independence

Syntholene’s branding is “Unlimited Fuel. Forever.” This reflects that each synthetic fuel facility doesn’t have any reserves that deplete like a traditional mine or oil rig. This is not just a value add for investors as assets retain value but gives countries energy independence - especially for Iceland, who currently is a net importer of liquid fuels.

Secured Expression of Interest for Off-take

Syntholene has secured an expression of interest with Icelandair for 250M litres of e-SAF over a 10 year period reflecting a contract value of $1.9B USD. Once their demonstration facility is operational, Syntholene should be able to provide samples of e-SAF to Icelandair to sufficiently satisfy their testing providing grounds to enter into a definitive off-take.

Favourable Access to Infrastructure/ Supply Chains & Skilled labour

The vast geothermal network of Iceland also situates Syntholene is an environment where there is a higher than average concentration of workers specialized in geothermal operations and, by extension, skilled in operating large complex thermo-chemical processes. Thus, it is likely that Syntholene will benefit from a skilled local talent pool for contractors and employees; instead of importing skilled workers.

Benefits to Customers & Substitution Threat to Fossil Fuels

Given that Syntholene’s e-SAF (and all e-SAF) has a 7% higher energy density and is cleaner to burn, there are direct benefits to airlines that use e-SAF over fossil fuels. If we assume equal pricing for e-SAF and fossil fuel derived aviation fuel:

average fuel savings of $2,682 USD on a single trip from London to New York. For a carrier with a $9 billion annual fuel expenditure, a major airline could see over $600 million USD in annual bottom-line savings

For a major airline, the transition to an ultrapure e-SAF like Syntholene acts as a "preventative medicine" for jet engines. My estimates show an annual maintenance savings per aircraft are about $643,500 per year.

Price stability. As mentioned by Syntholene’s CEO, syntholene will be able to provide long-term pricing that is disconnected from oil prices. This long-term pricing will be preferred by customers who are willing to pay up to ‘30% to 40%’ higher prices for stability.

Given the win-win-win nature of Syntholene’s e-SAF, it poses a long-term threat to fully replacing fossil fuel derived aviation fuel.

Potential Licensing

Sytholene’s CEO has mentioned that they will likely license the technology to some degree, in addition to, investing/use of special purpose vehicles for each project build out.

Macro Tailwinds and Government Incentives

There are numerous tailwinds that broadly support growth including subsidies for airlines using e-SAF, European grant programs (EU Innovation Fund and the European Hydrogen Bank) and, national subsidies/grant programs in IceLand.

By 2050, the demand for e-SAF will reach 22B litres annually. If Iceland tried to meet 20% of this supply, they will nearly double current GDP over the next 25 years (22B litres x $7.14/litre x 20% = $31.42B). This would make Iceland the wealthiest country in the world on a per capita basis. Realistically, for Iceland to produce 4.4B of e-SAF annually by 2050, they would need to more than double total electrical capacity from around 3 GW to 3.5 GW by 2050. This would also require total geothermal expansion of more than 4x its current size. So does Iceland choose to participate in these climate initiatives or do they leave it to other countries with more environmentally intrusive practices?

And for Europe too, this is a generational opportunity to reduce reliance on Russia and the Middle East for energy. And to quote one of the first Russians, Gorbachev: if not us, then who? If not now, then when?

RISKS: FINANCING; REGULATORY CHANGE; DISTRIBUTION

Syntholene is pre-revenue. As of January 2026, the company held 3.5M in cash. Dilution is an inevitability. They appear to need an additional $4M in funds to complete the demonstration facility. At current price levels, the dilution for the demo facility shouldn’t be harmful potentially in the range of an additional 8 to 10 million shares. The real financing and potential destructive dilution could occur financing the first commercial facility when Syntholene will need $200M-$250M. They hope to use a combination of equity and debt to finance the facility.

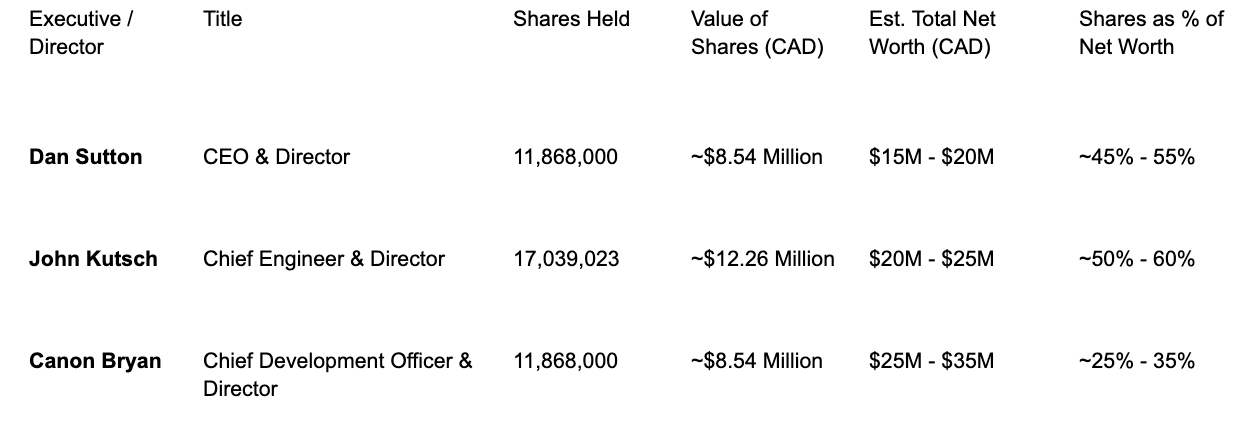

I find the only protection from highly dilutive financing is insider ownership. Syntholene perfectly exemplifies a leadership team putting skin in the game. I asked Gemini to estimate each founders net worth and conversely estimate how much of that net worth is in Syntholene:

I believe it is safe to assume that the founders and executive will avoid value destructive financing as much as possible given their skin in the game. Also, management acknowledging that R&D on reactor technology would be too expensive and value destructive at this stage leads me to believe they are conscious capital allocators.

Further downside protection is provided by the tight float. Insiders hold approximately 50-60% of shares with Shell also holding 8%. There are also long-term lock up periods preventing founders from selling shares. In an interview, Dan Sutton commented that the float is only about 25M shares. By having a tight float, the share price will be a less volatile to the downside as long-term investors slowly eat it up. Reduced share price volatility to the downside then permits raises at higher share prices thereby reducing the amount of dilution.

There is also execution risk. However, given they are simply creating new integrations for existing technologies and the experience of the team, I see execution risk as relatively low.

Regulatory policy shifts in the EU could also change demand and alter project economics. However, given that current policy is intended to provide stability for cap ex investment into renewable energy and e-SAF, I assess potential regulatory shift in Europe as low. Further, other jurisdictions are following Europe's moving toward subsidies and mandatory blends supporting demand.

Upcoming Catalysts and Events

Third-Party Validation and Techo-Economic Reports. Reports from Robert Raiper and Kellog, Brown, and Root are expected this year.

Additional Raise and Financing for the demonstration Facility;

Demonstration Facility Results

VALUATION

DCF Valuation

DCF valuations are not the holy grail. They are a tool that has many levers. Like any tool, its usefulness is based on how we pull those levers. Some assumptions I’ve used throughout this analysis are: 1) a stable e-SAF price of $7.16/litre; although, the structural deficit is likely to lead to higher prices; 2) terminal growth rate of 3%; although, Syntholene will likely be hitting an exponential growth rate by 2035 when they can fund their own cash flows indicating a much higher growth rate; 3) WACC/Discount Rate of 12%; 4) Syntholene’s op costs remain at 1.24/L of e-SAF; although, Syntholene has stated intentions to have a lower op cost at scale.

Examining the current market cap for Syntholene is instructive as to what future success the market has priced into the stock. Using a reverse DCF model, we can see that the terminal value largely carries most of the present day market cap for a 10 year DCF the market cap implies FCF of 10.6M in 2035. Given Syntholene’s first commercial module is expected in 2029 to generate approximately 20M/L e-SAF in 2030 at a $5.96/litre net profit, we would expect 119.2M in operating cash flows. With four additional facilities being built before 2035, there is potential for Syntholene to reach over $500M in recurring revenue by 2035. Thus, there is a disconnect between Syntholene’s Marketcap and plans for future revenue.

In terms of a 10 year DCF, current intrinsic value/NPV of future cash flows range from $2B to $3B with probable outstanding share count in the range of 200 to 300M shares. This implies that, with dilution, a share price of $6.66 to $15USD [$9.32 to $21 CAD]. Note, raising the discount rate to 18% reduces current intrinsic value closer to $1B Mcap. Rolling our DCF forward to 2030 assuming growth at 1 module/year, the intrinsic value/NPV of future cash flows range from $5B to $6B. This implies that the intrinsic value of the company will likely more than double by 2030. This also implies a share price of $16.67 to $30 USD [23.34 to $42 CAD] with 200 to 300M outstanding shares.

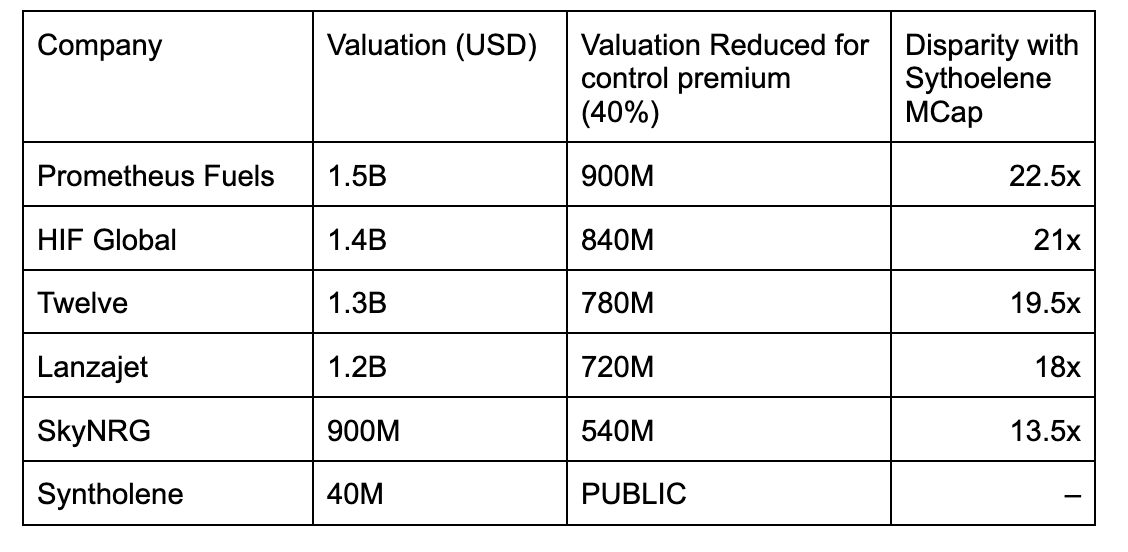

Valuation by Company Comparison

Below is a table of comparable SAF producers and their private valuations.

Discussion on Valuation

There is a significant disconnect between Syntholene’s corporate plan/future cash flows and its share price. The stock is essentially trading at 5% to 10% of intrinsic value/NPV.

In my experience, there are a few reasons for stocks to be so disconnected from intrinsic value: 1) the stock is currently priced for failure due to technological risk; 2) the cash flow is so far in the future investors remain sidelined similar to mining stocks pre-feasibility study; 3) Given the stock only started trading on December 12, 2025 and there is little to no marketing in Germany or the United States, I do believe that many people simply do not know or understand this stock. Thankfully, time will take care of numbers 2 & 3.

In terms of technological risk, I believe that investors' initial impression of Syntholene is that it is unproven and novel technology (this is what I thought initially). But since their production actually doesn’t use any new technology and just uses a new integration, technology risk is much lower than other clean technology companies. Further, there are upcoming milestones that I anticipate will reduce perception of a technology failure including: third party validation of techno-economic reports; and, completion of the demonstration plant. Each technology achievement will result in more success being priced into the stock.

Price Targets with Logic

12-18 month Target: $4 to $10 CAD

One year from now, the demonstration facility should be complete. We should also have economic data from the pilot plant that will, hopefully, confirm the op costs for the project. These accomplishments should largely derisk the investment for early investors. I do think this is also a story that is somewhat viral.

3 year Price Target: $8 to $25 CAD

Three years from now, Syntholene will either be operating its first commercial plant or close to completing construction. At this point, I would expect future revenues to be included in the market cap. Syntholene’s Mcap should at least match those of the private companies listed, above. I would expect early institutional investments and/or inclusion in some ETFs.

5 Year Price Target: $25 to $50++ CAD

Five years from now, Syntholene will have transitioned from pre-revenue into, hopefully, a business generating revenues. The technology and economics will be validated at scale. Given the high margins, unique value proposition and unusual long-term growth runway, there is the possibility it trades at a very high P/E well beyond intrinsic value.