A $500+ premium, fragmented markets and the quiet reconfiguration of copper dependencies

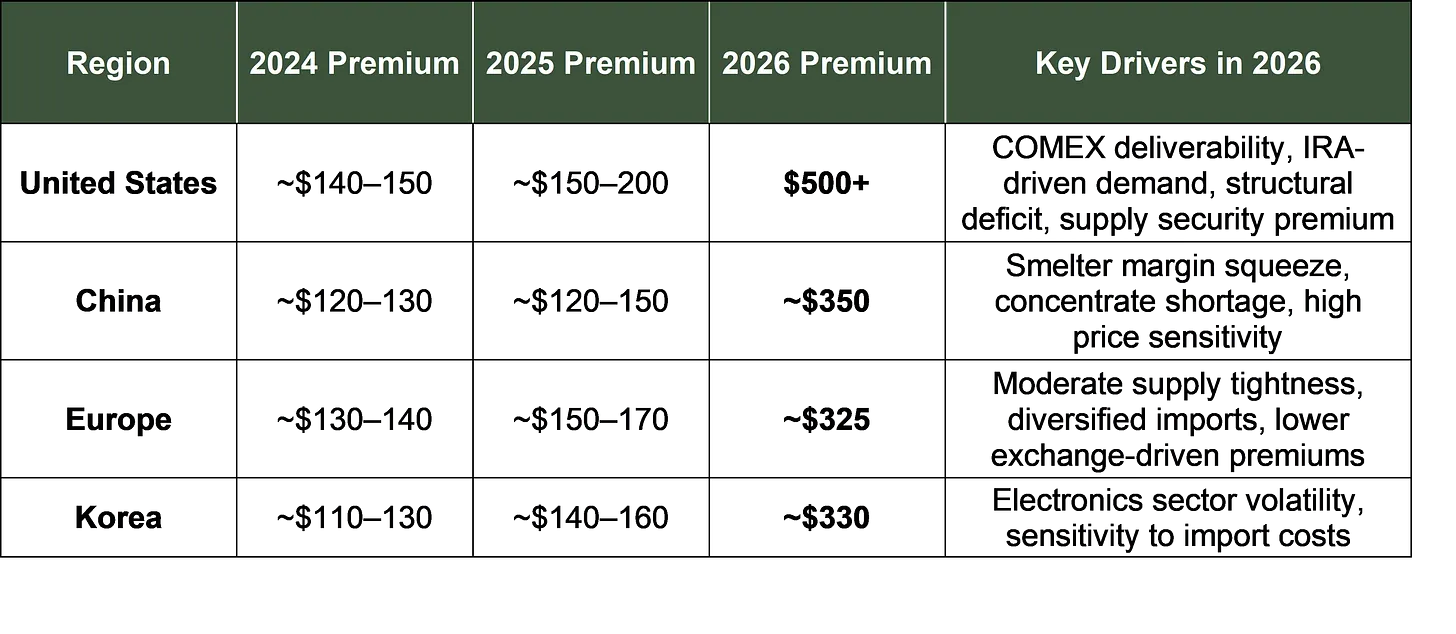

Looking at global copper markets through the lens of structural transformation, it is hard to avoid the feeling that copper has stopped behaving like a normal commodity. The record-breaking 2026 Codelco premiums – above $500 per tonne for U.S. buyers, versus roughly $350 for China and around $325 for Europe – are not just a pricing curiosity.

They mark a break with the past, where regional premiums moved in a tight band, and confirm a trend I explored in a previous piece on copper premiums and Geopolitical Mining: the physical “extras” around the LME price are becoming a proxy for power, dependency and strategic alignment in the copper system.

Link to previous article: https://edzamanillo.substack.com/p/copper-premiums-and-geopolitical

What Copper Premiums Actually Do

Copper premiums are the extra amount buyers pay on top of the LME benchmark price to secure physical cathode in a specific region. They typically cover:

Freight and insurance

Regional taxes and handling

Local supply–demand tightness

Sometimes, the value of exchange deliverability (COMEX or LME)

Premiums are the bridge between paper copper (LME, COMEX) and real copper (a cathode on a truck, a ship or in a rod mill). When LME prices touched around $11,200/t in late October 2025 and COMEX traded even higher, those regional premiums stopped being a footnote and became a core part of total delivered costs.

Historically, Codelco’s annual premiums to the U.S., Europe and China moved broadly together. The differences were there – logistics, local demand, currency – but the spread between regions was modest. That is what makes 2026 so striking.

What Changed in 2026? The New Premium Geography

For 2026, reports indicate roughly the following Codelco premiums:

In previous years, the U.S. and China were usually separated by a few tens of dollars per tonne, not $150+. The natural question is: if the “market structure” has existed for years, why does the gap explode now?

Three things have shifted simultaneously:

An unprecedented COMEX–LME price divergence

A policy-driven demand shock in the U.S. (IRA, grid, reshoring)

A severe concentrate and smelter-margin squeeze that bites China much harder than U.S. fabricators

Why the U.S. Is Paying $500+ While China Pushes Back

1. COMEX Deliverability Suddenly Has a Price

In mid-2025, COMEX copper futures traded almost $1,800/t above LME at the peak, an extraordinary spread by historical standards.

For U.S. buyers, Codelco cathodes are COMEX-deliverable. That gives them three layers of value:

A hedgeable, financially recognised asset

Eligibility for physical settlement on COMEX

Flexibility to arbitrage between physical and futures markets

In this environment, the premium is no longer just about freight. It is also the price of access to a financial and logistical safety net. China and Europe do not value COMEX deliverability the same way because they anchor on LME and Shanghai benchmarks instead.

2. The U.S. Demand Shock Is Policy-Driven and Inelastic

U.S. copper demand is being reshaped by:

IRA-related grid and renewables projects

Transmission upgrades

EV and battery plants

Semiconductor fabs and manufacturing reshoring

Many of these projects are backed by federal incentives and firm timelines. They are not easily postponed just because copper premiums feel uncomfortable. For these buyers, the relevant comparison is not between a $300 and $500 premium, but between:

Paying up for secure, Chilean cathodes

Or risking delays to multi-billion-dollar projects

In other words, U.S. demand for secure refined copper has become much less price-sensitive in the short term.

3. China’s Smelters Live in a Different Economic Reality

Chinese smelters, by contrast, sit at the other end of the chain:

They rely heavily on imported concentrate

They have seen TC/RCs squeezed by global disruptions

Their margins are thin and under pressure

They cannot simply pass higher cathode premiums through to end customers

Codelco’s offer of around $350/t for 2026 – up from about $89/t the prior year – has triggered open threats by some Chinese buyers to walk away from term contracts.

The key point: Chinese buyers can sometimes flex between concentrate, cathode, blister and scrap, and they are structurally more price-sensitive than U.S. fabricators who need high-quality, exchange-deliverable cathodes.

Logistics also play a role: Chilean cathodes move into the U.S. West Coast through one of the most reliable shipping corridors globally, with fewer geopolitical and port disruptions than Asia-bound routes. That reliability carries implicit value when buyers are prioritising supply certainty

Is Codelco “Abusing” Its Position – Or Is This Just the Market Talking?

From the U.S. perspective, a jump from roughly $150–200/t premiums in recent years to $500+ today looks brutal. But it does not automatically mean that Chile – or Codelco – is abusing market power.

A more realistic interpretation is:

U.S. buyers are not happy to pay $500+; they are choosing the least risky option in a system defined by tight supply, COMEX–LME dislocation and policy-locked demand.

Codelco is behaving like a rational producer with limited volumes and multiple competing outlets, pricing most aggressively where its material has the highest strategic value:

COMEX deliverability

Strong legal and logistical links

Deep demand related to industrial policy

This is consistent with the logic I discussed previously around speed vs tonnage and the midstream leverage of state-linked players: in tight markets, pricing power flows towards whoever can deliver secure, fungible, high-quality units into the most politically constrained demand pool.

Chile–U.S. Relations: Strategic Alignment or Future Friction?

High premiums do more than move balance sheets. They alter perceptions.

On the U.S. side, paying the highest premium in the world to a single supplier reinforces three ideas:

Chile has become a strategic node in U.S. copper security.

Refined copper is now closer to a strategic input than a generic commodity.

Some degree of structural dependency on Chile is being priced in.

This sits on top of a relationship that already includes points of friction: debates around Chilean mining taxation and royalties, environmental and water constraints, lithium policy uncertainty, and the broader question of how Santiago balances its ties with Washington and Beijing.

These dynamics unfold at a time when the political tone between Washington and Santiago has, on occasion, shown signs of misalignment. Even when the institutional relationship remains strong, diplomatic nuance can influence how supply-chain dependencies are perceived and managed, adding a layer of sensitivity that is not present in purely commercial markets.

From Chile’s side, elevated premiums improve Codelco’s cash generation at a time when the company is under pressure to finance both heavy reinvestment and the state’s broader fiscal needs. But higher leverage also means higher expectations:

If strikes, droughts or project delays curtail Codelco’s output, this will increasingly be read in Washington as a strategic risk, not just a domestic operational issue.

If Santiago leans further into resource nationalism or regulatory tightening, it could be framed as weaponising a critical supply node – fairly or not.

The risk is not immediate confrontation, but a subtle shift: copper starts to appear on the bilateral agenda, not just on invoices.

What Happens Next Year? Three Signals to Watch

No one knows where 2027 premiums will land, but a few markers are worth tracking.

1. Does the U.S.–China Premium Gap Narrow or Widen?

If the gap between U.S. and Chinese/European premiums narrows, it will suggest that:

COMEX–LME spreads are normalising

Some supply bottlenecks are easing

Chinese resistance is having some effect

If the gap widens, U.S. political actors may increasingly view the premium structure as a form of geo-economic rent extraction, even if the underlying drivers remain fundamentally commercial.

2. Does China Walk Away From Codelco as Benchmark?

Chinese buyers are already questioning whether Codelco’s annual term deals still reflect their reality. Persistent friction could push them to:

Rely more on spot markets

Anchor on alternative benchmarks

Use more diversified sourcing and recycling

That would weaken Codelco’s traditional role as a global reference point and fragment pricing further – an outcome very much in line with the Geopolitical Mining narrative of regionalised, politicised commodity systems.

3. Does the U.S. Double Down on Domestic and Regional Supply?

A sustained period of $500-type premiums will strengthen arguments in Washington for:

Fast-tracking domestic mining and permitting reform

Deepening copper ties with other suppliers (Canada, Mexico, perhaps new projects in the Americas)

Supporting new smelting and refining capacity closer to home

If the premium structure of 2026 persists or intensifies, it becomes a powerful data point for those arguing that the U.S. cannot rely indefinitely on imported refined copper, even from friendly states.

This tension is not new. In a piece I wrote in July on whether the U.S. could offset the copper tariff shock through domestic production, I argued that the United States simply does not have the geological inventory, permitting velocity or smelting capacity to close its structural deficit in refined copper. Even under optimistic scenarios, U.S. production growth in the coming decade falls well short of projected demand driven by grid upgrades, semiconductors, and EV manufacturing. The premium spike of 2026 reinforces that conclusion: Washington can accelerate permitting, support Arizona and Utah expansions, and deepen ties with Canada and Mexico, but it cannot meaningfully detach from refined imports. High premiums do not just reflect market tightness — they expose the limits of U.S. copper self-sufficiency (in the short-medium term).

Link to previous article (on July): Can the U.S. Offset Its Copper Tariff Shock? A Closer Look at Domestic Levers

Conclusion: Premiums as a New Language of Power

Codelco’s record 2026 premiums are not an isolated spike. They crystallise several deeper shifts:

From cost optimisation to security of supply

From globally integrated pricing to regionalised, structurally divergent premiums

From copper as a neutral commodity to copper as a carrier of industrial strategy and geopolitical alignment

For buyers, this means rethinking contracts, hedging and inventory strategies in a world where the “extra” over LME can be as politically charged as the underlying price itself.

For Chile and the United States, it is a reminder that what appears to be a commercial detail – a $500 premium instead of $300 – can quietly reshape patterns of dependence, leverage and strategic expectation in the global copper market.