A Cashed-Up Junior With Heavyweight Backers - (CSE: NOM, OTC: NRRSF, FWB: LXZ1)

In junior mining, credibility comes down to who is standing behind the project. Norsemont Mining has attracted an elite roster of backers rarely seen together in one deal:

Rob McEwen – legendary gold investor, founder of Goldcorp

Dr. Quinton Hennigh – globally recognized exploration geologist

Crescat Capital – known for high-conviction mining investments

Lawrence Lepard – hard money fund manager and vocal gold bull

Paul Matysek – serial entrepreneur who has built and sold multiple billion-dollar mining companies

When industry titans like these put their own money into a story, it sends a strong signal. They see Norsemont’s flagship Choquelimpie Gold-Silver-Copper Project in northern Chile as a project with the potential to become a mine again.

Why Choquelimpie Matters

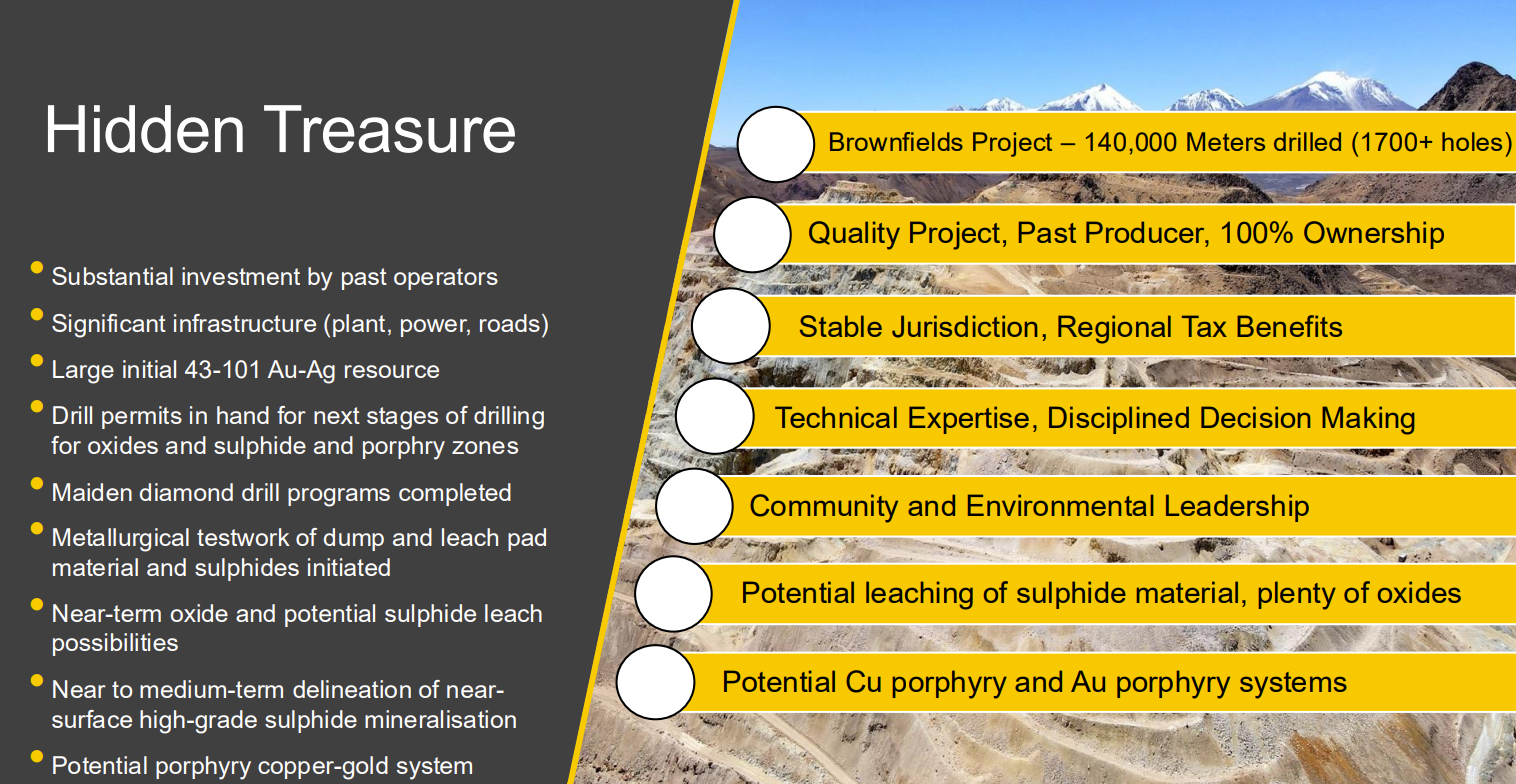

Choquelimpie is not just another greenfield play. It is a past-producing mine that was historically the third largest gold producer in Chile, producing more than 415,000 ounces of gold under previous operators.

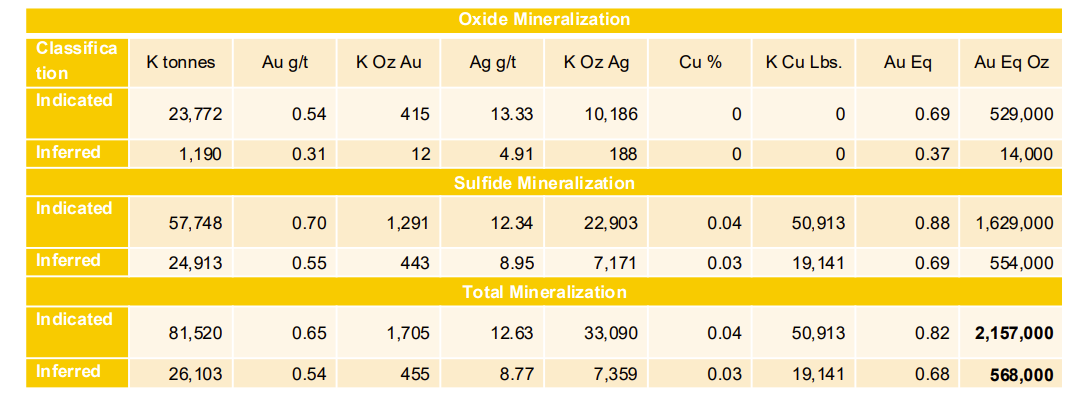

Today, Norsemont controls 100% of the 5,757-hectare project. It already carries a 2.74 Moz AuEq NI 43-101 resource (Indicated + Inferred) with substantial growth potential.

Key assets already in place:

3,000 tpd mill

Power, water, and permits

Fully equipped camp, offices, and warehouse

ADR treatment plant and lab facilities

For a junior explorer, this infrastructure represents tens of millions of dollars in sunk costs that don’t need to be replaced.

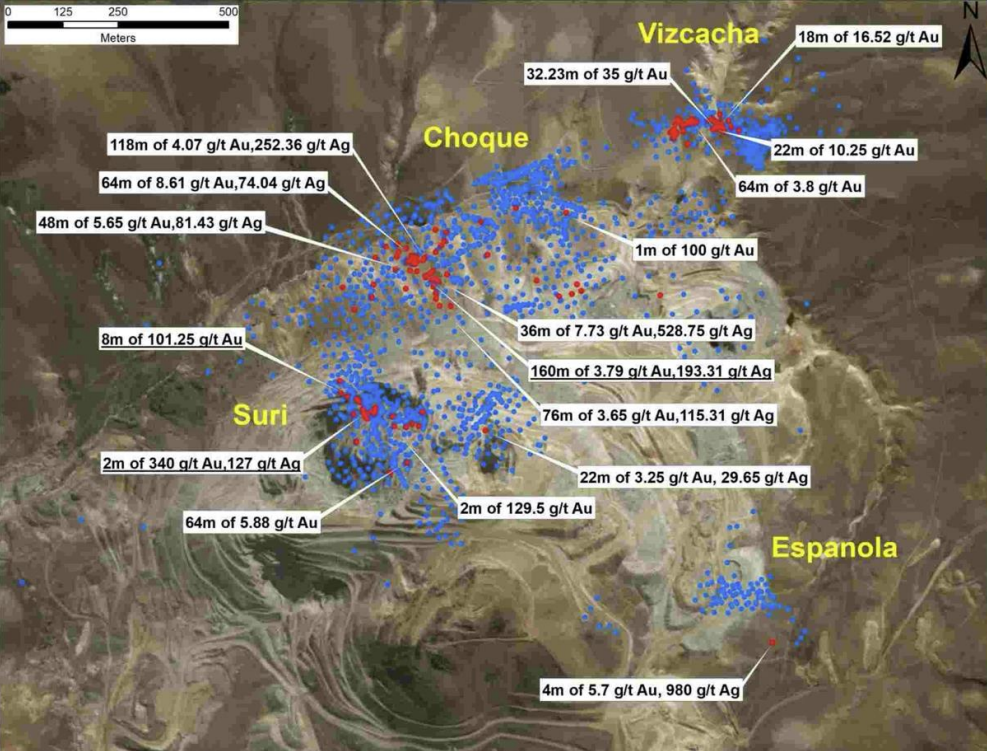

High-Grade Historical Hits

The project is defined by exceptional historical drilling. Many holes ended in mineralization, showing an open system. Highlights include:

35m @ 32.2 g/t Au (A-327) (Confirmed by re-assay)

158m @ 3.9 g/t Au & 200 g/t Ag (R-002)

24m @ 38.0 g/t Au & 148 g/t Ag (R-579)

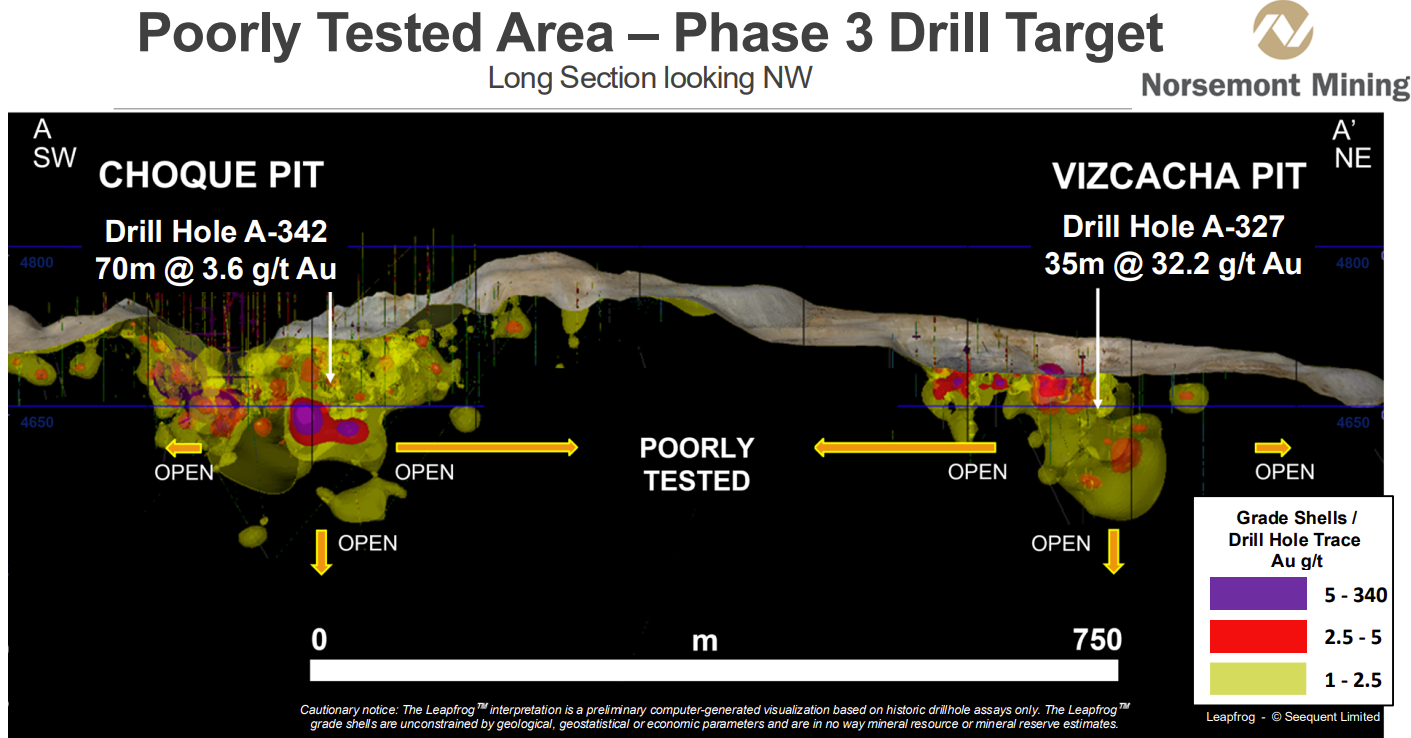

There are 140,000 meters of historical drilling across 1,700+ holes, yet most were drilled only to shallow depths of 70–80 meters. The deeper porphyry copper-gold system remains virtually untested.

Most of Choquelimpie’s historic drilling only went down 70–80m and bottomed in mineralization. This central zone remains poorly tested and leaves huge upside potential as Norsemont steps out and drills deeper for the copper-gold porphyry system.

Oxide Upside and Near-Term Production

Norsemont holds 540,000+ AuEq ounces in oxides with excellent historic heap leach recoveries up to 90%.

Stockpiles and leach pads add another ~210,000 AuEq ounces sitting at surface.

At today’s $3,500+ gold price, the economics are highly attractive. Oxides represent a clear, low-capex path to near-term production while the company advances the much larger sulfide and porphyry potential.

One of the Cheapest Valuations in the Sector

Norsemont trades at a market cap of only $60M CAD ($44M USD) with 2.74 Moz AuEq resources.

At today’s gold price of $3,559/oz, that resource equates to a notional in-ground value of:

2,740,000 oz × $3,559 = $9.75 billion USD

Norsemont’s valuation represents only about 0.05% of that figure...

Yes, more work needs to be done and there will be costs to advance the project, but this is still one of the cheapest advanced-stage juniors in the sector.

And this is only based on the current 2.74 Moz AuEq. In 2017, a non–43-101 estimate suggested 5M+ ounces at Choquelimpie. Expanding back to that level with improved grades looks realistic with drilling.

If the deeper copper porphyry system is proven out, it could completely re-rate the company and put it in the crosshairs of majors.

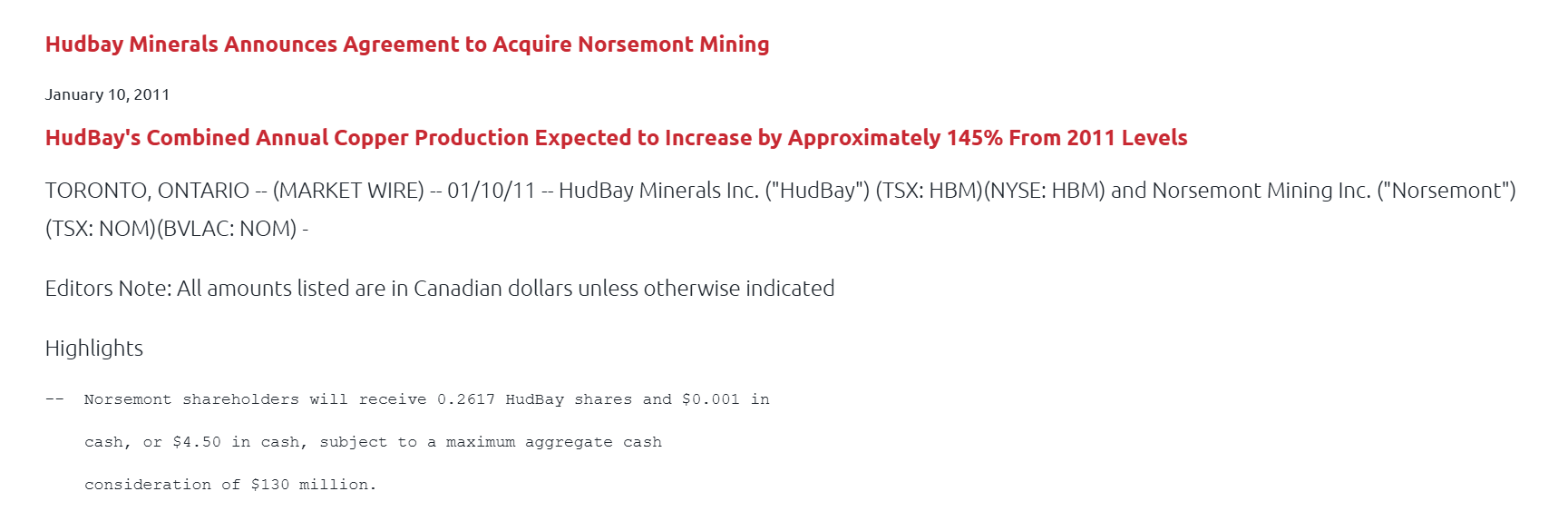

It’s also worth remembering that Marc Levy was part of the team that discovered the Constancia deposit in Peru, which Hudbay later bought and built into one of the world’s largest copper mines. Given that history, I would bet Marc’s real vision is to make Norsemont a cash-flowing machine rather than a quick flip. The valuation of a producer is far superior to a takeover, and a mine like Choquelimpie could live on for decades.

With infrastructure already on site and heavyweight backers aligned, Norsemont looks like one of the best risk-reward setups in this gold bull market.

Skin in the Game: Marc Levy’s $9M+ Commitment

Chairman & CEO Marc Levy previously built the original Norsemont Mining into a $520M buyout by Hudbay.

This time, Marc and his family have personally invested over $9 million into the company. That kind of skin in the game means they don’t have the option of failure. Their success is tied directly to shareholders’ success.

Betting on Teams Who Have Done It Before

I have seen countless juniors over the years. Most never deliver. But Norsemont offers the rare combination of:

A past-producing mine with ounces in the ground

Elite backers who have built billion-dollar companies

Cash in the treasury and drill ready

Management with a track record of exits

In my view, Norsemont has a better chance than 99% of the juniors in today’s market. Even respected commentators like Don Durrett, John Feneck, and Allan Barry Laboucan see the scale of the opportunity.

Conclusion: Positioned for the Bull Run

Gold is trading at record highs above $3,500. Supply is constrained, and majors are hunting for projects with size, grade, and infrastructure.

Norsemont Mining checks every box:

Cashed up and ready to drill

Tight structure with insider alignment

Historical mine with real production pedigree

High-grade drill results and oxide cash flow potential

One of the lowest $/oz valuations in the sector

In my view, this is not just another explorer. Norsemont could realistically transition to production in the next few years, while delivering leverage to gold, silver, and copper in the process.

Norsemont Mining will be the next great Chilean mining story.

Sincerely,

Mr. Uppy

Disclaimer

This article is for informational purposes only and not investment advice. Do your own due diligence (DYODD).

I personally own shares of Norsemont Mining. I am not compensated by the company in any way. I believe this project has the potential to become a producer and a major win for shareholders and hence why I want to share it with the world.