A Past Producer the Market Completely Forgot (CSE: FNAU | OTC: FNAUF)

In junior mining, the best setups are often the ones the market has completely forgotten.

Four Nines Gold is one of those stories right now.

This is not a grassroots explorer. It is a past producing gold mine in California that has already produced over half a million ounces of gold, then sat idle for decades while the real upside may have been left behind.

And I already know what you’re thinking: who the fuck is going to get a mine permitted in California? Yet little did you know and before I deep dove into this that California is actually the 4th largest mining district in the USA. And if you don’t believe me, ask Google:

Now the company is coming back with a completely different geological model and targeting what the previous operators missed.

Why Hayden Hill Matters

The Hayden Hill Gold Silver Project sits in Lassen County, California, a jurisdiction that rarely offers this kind of setup. This sparsely populated region in northeastern California leans strongly conservative, with Trump receiving 72% of the vote in the election (2016) and over 80% in 2020.

This is not a theory. This is a real mine with real history.

~483,000 ounces of gold produced and roughly 127k from pre-1976 mining

~1.34 million ounces of silver produced

Open pit mining from 1992 to 2000

Before that, the story goes back even further.

Gold was first discovered at Hayden Hill in 1870, with underground mining from high grade quartz veins continuing through the 1920s. Historical production from that era is estimated at 127,744 gold equivalent ounces, primarily from the Golden Eagle and Juniper zones.

This is a system that has produced gold across multiple generations of mining.

And despite all of that, it has not been properly explored in nearly 30 years.

The Missed Opportunity

The previous operator approached Hayden Hill as a bulk tonnage, low grade heap leach.

Average drill depth was about 150 meters

Focus was shallow mineralization

Mining largely stopped above higher grade zones

But here is what makes this situation unique.

This is not a project that lacked work.

There are hundreds of thousands of feet of historical drilling, representing well over 100,000 meters across more than 700 holes.

The issue was not the amount of data.

It was how that data was interpreted.

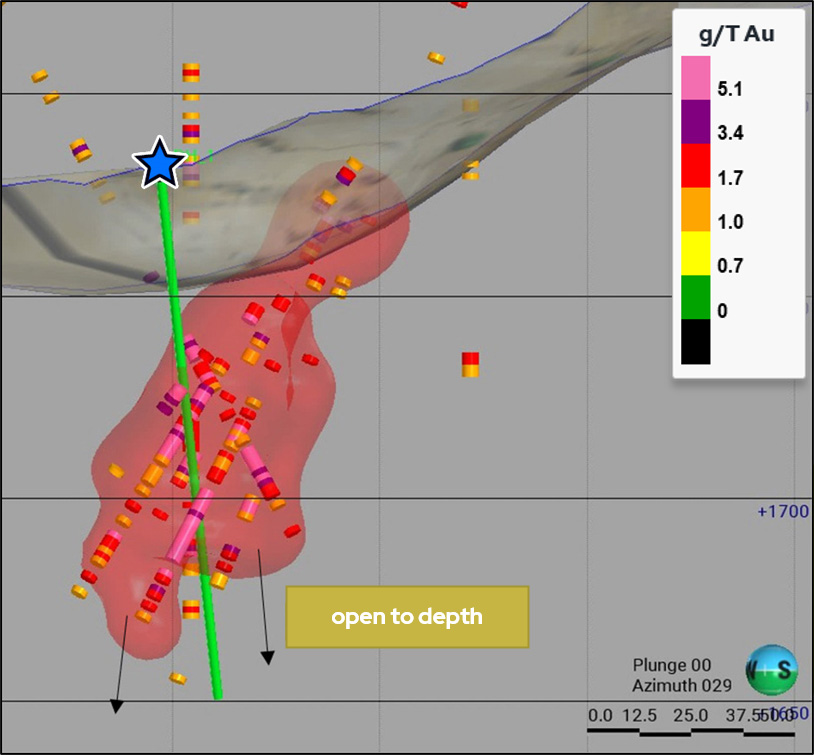

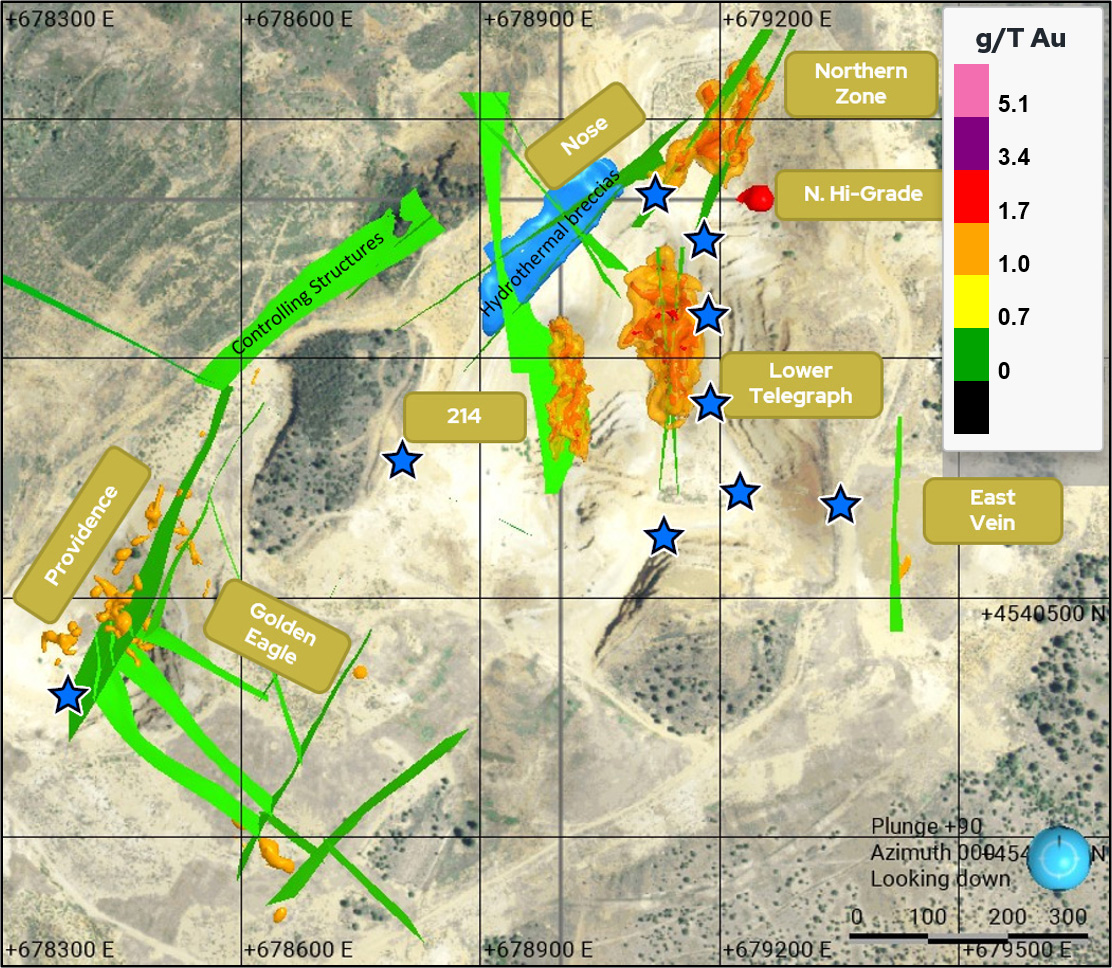

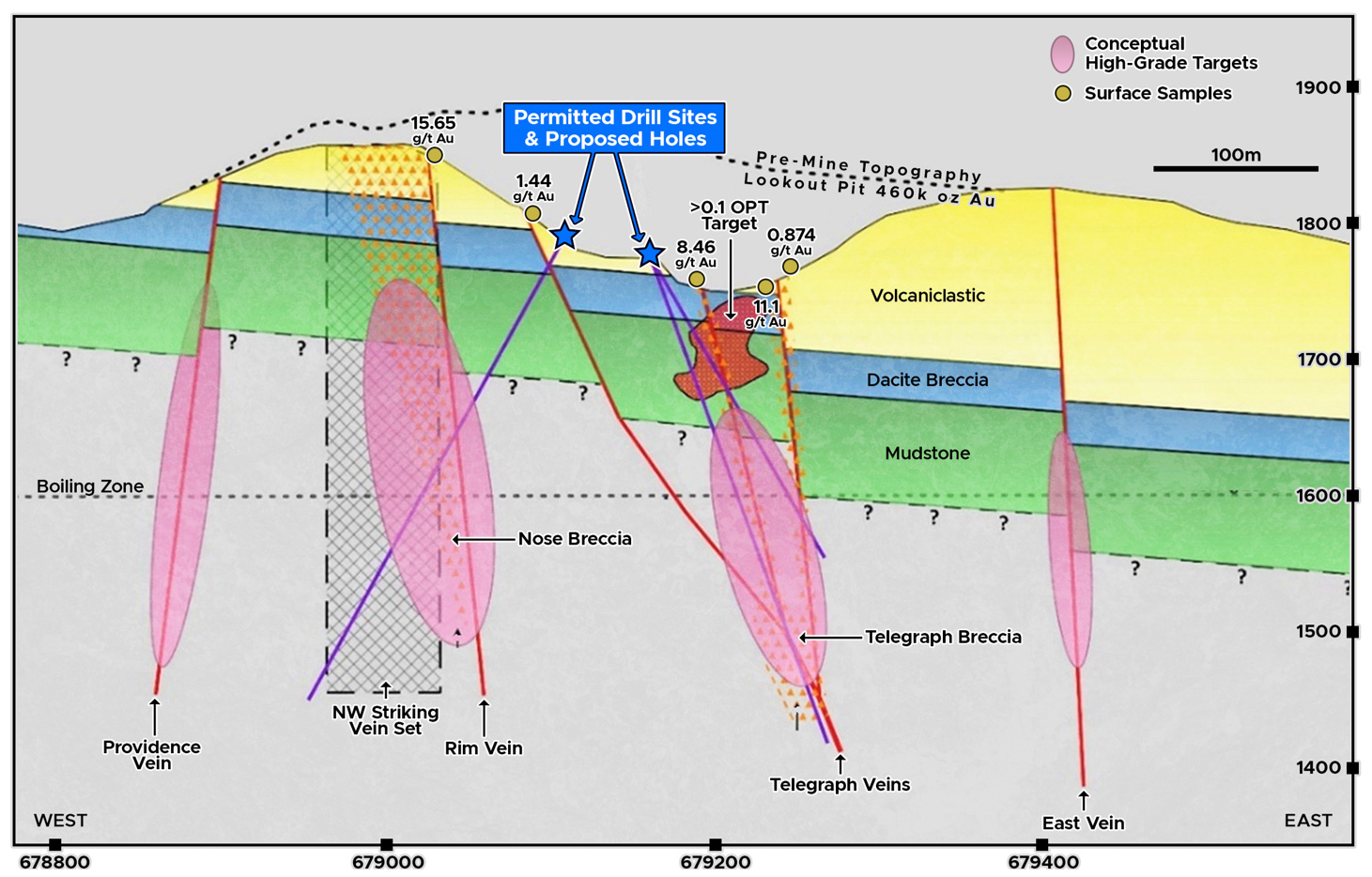

Gold here is structurally controlled.

Veins come together at depth around 200 meters.

High grade zones likely sit below and outside the pits.

So while a massive amount of drilling was completed, most of it:

Did not target the feeder structures

Did not go deep enough

Was not designed around a structural model

They mined what was easy to see.

Not necessarily what matters most.

The New Model: High Grade at Depth

Four Nines rebuilt the project using modern 3D modeling and a low sulfidation epithermal framework.

The thesis is simple.

The high grade feeder system was never properly targeted.

Historical drilling already hinted at it:

62.5m @ 10.6 g/t Au (Insane historical hit)

21.3m @ 7.5 g/t Au

15.2m @ 5.4 g/t Au

13.7m @ 12.0 g/t Au

These are not normal results for something that gets ignored.

They just were never followed up properly.

There is also a historical, non compliant resource of roughly ~2 million ounces, of which about 480,000 ounces were mined.

That leaves a large system that was only partially extracted and never fully understood.

The Plan: Go Where No One Drilled

The current permitted program is built to test that exact idea.

Up to 25,000 feet of drilling

Hole depths between 100 and 400 meters

Targeting high grade feeder zones

Focus on structural intersections

But there is another layer here that matters just as much.

The company is also going back into known mineralized areas to reconfirm and validate the historical, non compliant resource.

A large amount of historical drilling and production data exists, but much of it cannot be relied on today without modern verification.

So the strategy is twofold:

Step out and test the high grade targets at depth

Re drill and confirm known zones to support a modern resource

That combination of upside and de risking is what you want to see.

Past Production & Metallurgy

Hayden Hill was not just explored. It was mined at scale.

Total historical production reached:

483,060 ounces of gold

1,338,939 ounces of silver

Metallurgical performance was also strong.

Amax reported mill recoveries of 89.5% for gold and 59.3% for silver, at average grades of 0.087 oz per ton gold (~3g/t) and 0.381 oz per ton silver.

That is a key detail.

This was not a complex or marginal system. It was a workable deposit with solid recoveries, which is why it was mined in the first place.

Capital Structure & Recent Financings

This is where the story gets particularly interesting from a market perspective.

Over the past several months, Four Nines has completed approximately C$7.9 million in financings, bringing in a mix of strategic mining investors, European capital, institutions, high-net-worth investors, and insiders to fund the advancement of Hayden Hill.

The first financing raised approximately C$3.6 million at $0.20 per share with a half warrant at $0.35 and was reportedly oversubscribed with demand exceeding C$11 million.

More recently, the Company closed a C$4.3 million financing at $0.35 per share with a half warrant at $0.60, attracting strategic investors from Canada, Europe, the United States, and offshore jurisdictions.

Management and directors participated alongside investors and collectively own approximately 15% of the Company, creating strong alignment with shareholders. The shareholder registry now includes several strategic investors, including groups holding meaningful ownership positions, resulting in a tightly held structure with limited available float.

Updated Capital Structure

Shares Outstanding

74.8 million shares

Warrants

15.2 million warrants

Exercise prices ranging from $0.35 to $0.60

All currently in the money

Options

4.6 million options

Fully Diluted Shares Outstanding

94.6 million shares

Potential Additional Capital

Approximately C$7 million could flow into treasury through warrant exercises

Why It Matters

While the headline fully diluted number is approximately 94.6 million shares, investors should recognize that over 15 million of those shares are attached to warrants that would generate roughly C$7 million of additional capital for the Company upon exercise.

In other words:

Current shares outstanding: 74.8 million

Recently raised: ~C$7.9 million

Potential warrant proceeds: ~C$7 million

Potential total capital available: ~C$15 million

Fully diluted share count: 94.6 million

For a former-producing gold project with drill permits in hand, a fully funded drill program, significant insider ownership, and a growing roster of strategic shareholders, Four Nines remains relatively tightly structured compared to many junior gold exploration companies trading at similar valuations.

The Team: Built to Find What Was Missed

In early stage stories, the model matters.

But the people applying that model matter even more.

Four Nines has put together a team that is specifically built for this type of opportunity.

At the center of it is David Flint, who has led the technical work and 3D modeling that reshaped the understanding of Hayden Hill.

Chuck Ross, CEO of Four Nines and current CFO of Norsemont, alo brings over 30 years of experience in the resource sector, with a background spanning corporate finance, project oversight, and public company management.

The team also includes Art Freeze, a veteran geologist with deep experience in epithermal gold systems, and Dennis McHarness, former VP of Global Lands at Kinross, who brings nearly three decades of experience in mineral exploration, land strategy, and asset development across major gold systems.

Another key addition is Dr. Adrian King, former Head of Global Exploration at Teck, bringing major company discovery experience to the group.

There is also strategic oversight from experienced operators like Jim Mustard. Jim brings a rare mix of technical and market experience, with a background at operators like Barrick, Eldorado, and Amax, alongside senior roles in mining finance at Haywood and PI Financial.

And one detail that should not be overlooked.

This asset came from Kinross, one of the largest gold producers in the world.

Kinross completed full reclamation of the site and maintained it for years, leaving behind a historically clean footprint and extensive dataset.

This is not a greenfield discovery.

This is a known system that a major once operated, but never fully explored.

The Setup & Why This Could Re-Rate

This is where the opportunity starts to get interesting.

Today, investors are getting exposure to:

A past-producing gold mine

Located in California, one of the world's most valuable gold belts

A new geological model targeting higher-grade mineralization

A fully funded drill program

Permits already in hand

A micro-cap valuation

To put that into perspective, there are California gold stories trading at significantly higher valuations despite being at similar or earlier stages of development.

Apollo Silver currently commands a market capitalization of approximately $211 million.

Dateline Resources has reached a market capitalization of roughly $700 million.

K2 Gold has previously achieved substantial valuation growth based largely on exploration success, despite permitting challenges.

Four Nines sits in a very different position.

It already has:

A former-producing gold mine

Nearly 100,000 metres of historical drilling

Existing roads and infrastructure

Private land ownership

Drill permits already in place

A low-impact drilling program ready to go

That combination is rare.

Most junior explorers spend years and millions of dollars trying to secure permits, build a geological database, and prove a project has scale. Four Nines is starting with many of those boxes already checked.

The market is currently valuing Four Nines at roughly $35 million, which leaves considerable room for a re-rating if upcoming drilling validates management's geological thesis and demonstrates the scale investors are looking for.

The comparison isn't meant to suggest Four Nines should trade at Apollo's or Dateline's valuation today. Rather, it highlights the kind of valuations the market has recently assigned to compelling California gold stories when exploration success, project scale, and investor attention begin to align.

The Speculative Angle

This is still early.

There are real risks:

Historical data needs validation

No modern resource yet

Everything depends on drilling

Even the technical report highlights that new drilling is required to confirm and validate the dataset.

That is exactly why the opportunity exists.

The Bet

Old mine.

New model.

No attention.

If drilling confirms continuity at depth and the twinned holes match historical, this does not stay a microcap for long.

Bottom Line

Four Nines is not trying to find gold.

It is trying to find what was already missed.

A past producing system.

High grade already in the data.

And nearly 30 years without proper follow up.

Now it comes down to the drill bit and the team to execute.

Sincerely,

Mr. Uppy

Disclaimer

This article is for informational purposes only and should not be considered investment advice, a solicitation, or a recommendation to buy or sell any securities. Junior mining stocks are highly speculative and involve significant risk, including the potential loss of capital. Always do your own due diligence and consult with a licensed financial advisor before making any investment decisions as some information may be outdated or unreliable.

I personally own shares of Four Nines Gold ($FNAU) and may benefit if the share price appreciates. I have not been paid or compensated by the company in any way to write this piece. The views expressed here are entirely my own and reflect my personal opinion as a speculative investor.

Sources:

https://www.fourninesgold.ca/

https://www.fourninesgold.ca/files/FNAU_HaydenHill_43101.pdf

https://ceo.ca/@accesswire/four-nines-gold-closes-43-million-non-brokered-private

https://www.fourninesgold.ca/FNAU_Presentation_Web.pdf?74d79

https://www.asrs.us/wp-content/uploads/2021/09/0551-Williams.pdf

https://www.voanews.com/a/trump-enjoys-stong-support-in-lassen-county-california/4171579.html

https://www.nytimes.com/interactive/2021/upshot/2020-election-map.html