Fed members remain deeply divided — not only over what to do next on monetary policy, but also over the wisdom of their latest move.

The U.S. central bank cut interest rates by a quarter percentage point, as expected, lowering the target for its key lending rate to a range of 3.5% to 3.75%, the lowest since 2022. Yet the decision also signaled that the path toward additional cuts may be more complicated.

In the weeks leading up to the announcement, top Fed officials displayed an unusual degree of public disagreement. Three of the 12 voting members on the Federal Open Market Committee dissented from the quarter-point rate cut, the highest number of dissenters since 2019.

For now, further action appears unlikely. Chair Jerome Powell emphasized that the Fed is now "well positioned to wait" and observe how the labor market and inflation evolve before making its next move.

Recent data have offered a mixed picture. Inflation has picked up in recent months, even as hiring has slowed, raising concerns about potential stagflation. This puts the Fed in a difficult position as it attempts to balance its dual mandate: maintaining price stability and promoting maximum employment.

The central bank’s primary lever for addressing both challenges remains interest rates. If the Fed holds interest rates steady as a means of protecting against tariff-induced inflation, it risks a deeper slowdown of the labor market. However, cutting rates to stimulate hiring could spur spending and worsen inflation.

December’s meeting capped a difficult year for Fed officials — one marked not only by economic uncertainty but also by a series of personal attacks from President Donald Trump.

Financial markets reacted quickly to the latest decision. The EUR/USD pair jumped above $1.17 after the Fed delivered its third consecutive rate cut, sending dollar traders scrambling to interpret the signal: Was the move dovish, hawkish, or some uneasy mix of both?

The move pushed the pair to a three-week-high, near $1.1707, as the dollar struggled with conflicting policy signals and the euro extended its steady climb from December.

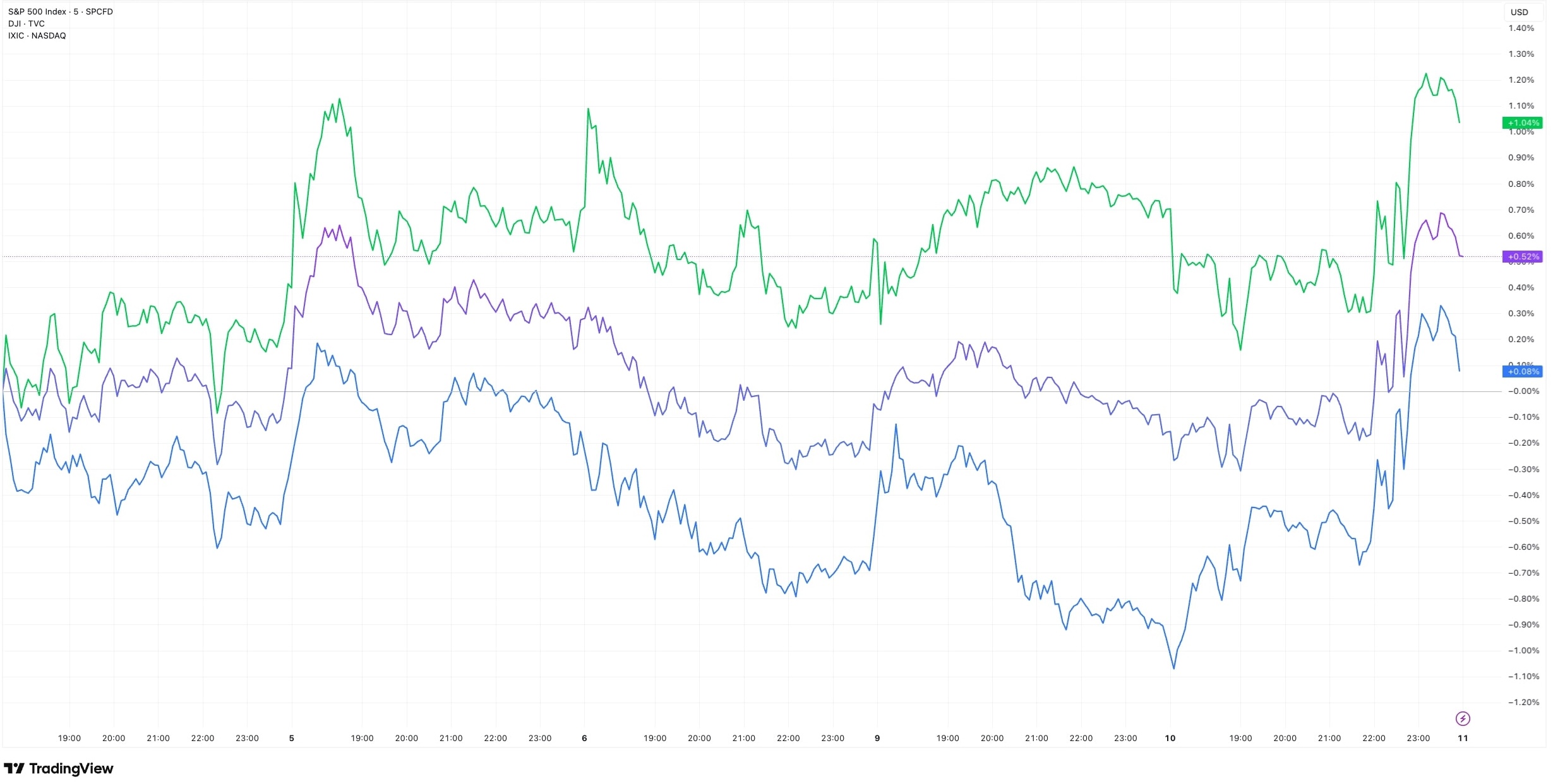

Equity markets responded as well. The S&P 500 rose 0.7%, the Dow Jones gained 1%, while the Nasdaq lagged but still managed a gain.

Sentiment improved after Powell acknowledged “significant downside risks” in the labor market.

However, new Fed projections point to caution about additional rate cuts next year, setting the stage for even greater tension between the Fed and the White House. For months, Trump and his allies have publicly attacked Fed officials. Despite elevated inflation, the president has continued to insist that any price increases are a lingering effect of the Biden era — even as some corporate leaders attribute recent price increases directly to tariffs.

Looking ahead, political pressures are likely to intensify. Powell’s term as chair will be up in May, allowing Trump to nominate a successor for the most influential economic role in the country. He has said he will announce his choice “probably early next year,” with National Economic Council Director Kevin Hassett emerging as an early favorite.