I had the opportunity to travel up to BC this past month to attend the 2024 AME Roundup conference held, as usual, at the beautiful Vancouver Convention Centre complex. My plan was to attend the first two days at AME, and with VRIC overlapping on the Monday, I was able to bounce back and forth between the two events and take in as much as possible. Vancouver is such a lovely city and when I visit there, I always allow myself to wander around a bit wide-eyed and just pretend that I am arriving in the city for the first time. I spent the majority of the first day on the VRIC exhibit floor, perusing the booths and dropping in on some of the talks. I made my way over to the Discovery Group booth and had the pleasure of speaking with Todd Hanas, VP of Investor Relations for Defense Metals, Jim Paterson, cofounder of Discovery Group and the Chairman and CEO of Valore Metals, and Nancy Curry, VP of Corporate Development for Kodiak Copper. Matthew Mickleborough of Junior Resource Investing stopped by the booth while I was there and we later spent some time sitting at the food court, talking about investing strategies and the condition of the markets for the juniors. The topic inevitably shifted to Kodiak, with both of us making the observation that it seems that many junior resource investors over-trade their positions, looking to get in and out to capture those brief upticks on the Lassonde curve. Few seem to want to find a good story, with a good project, run by good management, and stick with the investment over the long haul. Newsletter writers can reinforce the trading behavior, and accentuate the volatility. Kodiak's share price is currently sitting in the mid 30 to low 40 cent USD range, after starting out 2023 just under 0.95 USD, despite the building story of a promising district-size mineralization. Investor impatience and the generally poor resource markets have contributed to lower junior share prices across the board. I reiterated to Matthew that Kodiak, in particular, seems very undervalued and that I had been diligently building a large position. This is in light of what I see as compelling prospects for the company, with the excellent management team, the large and growing pipeline of targets and the careful methodology they are following.

In the afternoon, I headed across the causeway to Roundup and eventually got into the Core Shack and had excellent discussions with the Kodiak field team with insights on the recent drill season, water issues, the regional geology, and prospects for the South zone. The team is an impressive group of individuals, and I came away with a much better overall picture of the MPD project and priorities. I spent the rest of Monday visiting around the floor and came back to the Kodiak later on Tuesday with a new round of questions regarding the South Zone, which Dave Shelton, VP of Project Management, graciously spent time answering. What I came away with was a confirmation as to what a major deal the South Zone results were, despite the market discounting the 1 km long interval of 0.17% copper. The fact that they were able to hit such a long interval on the first try on a brand new target is extremely significant. This was further reinforced during a discussion that I had the next morning over at Kodiak headquarters with Claudia Tornquist, President and CEO.

Figure 1: Kodiak Copper Booth at the Roundup Core Shack

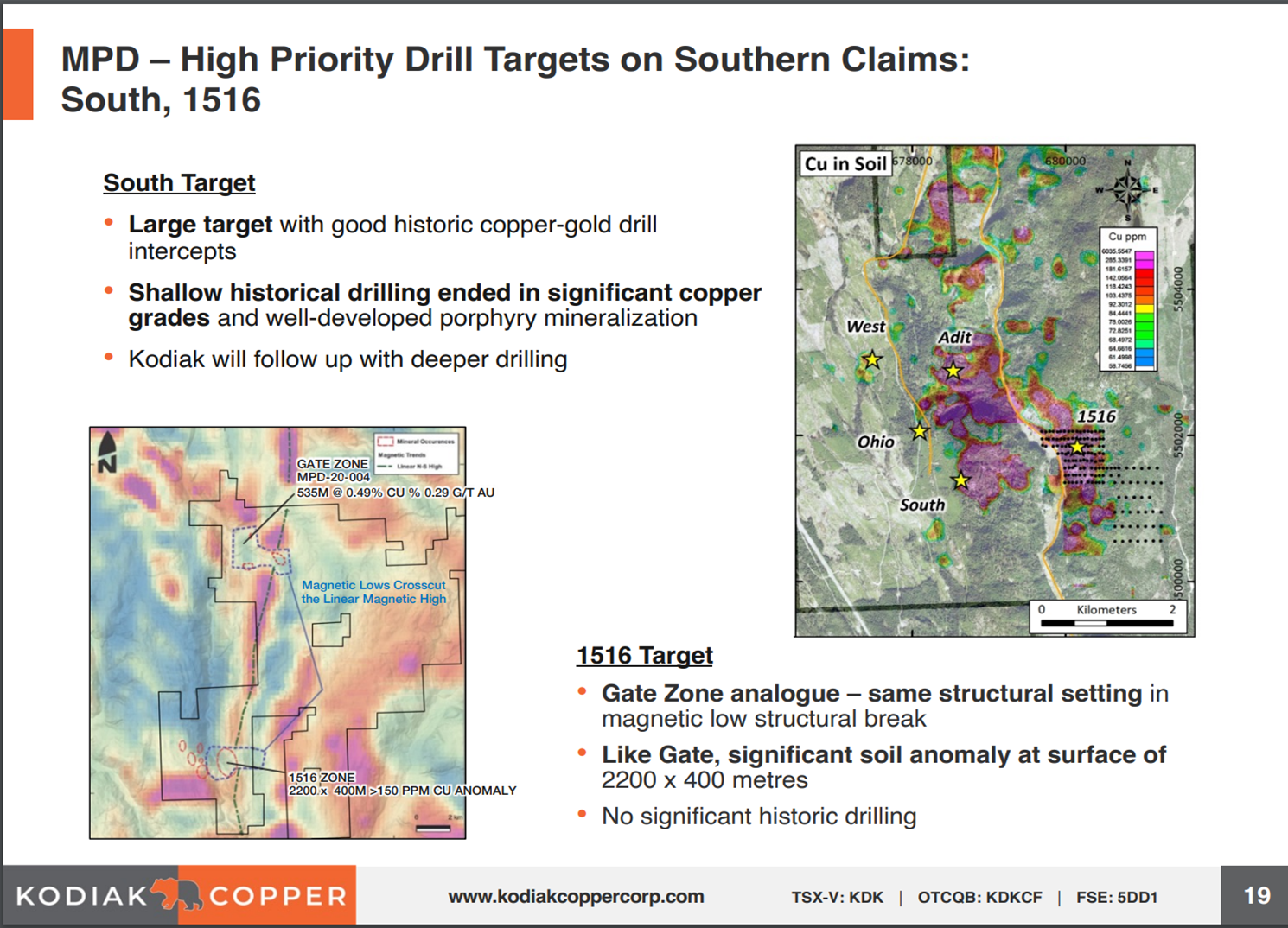

MPD South is potentially looking like one giant system, with the exception of the 1516 Zone. 1516, in particular, looks tantalizing due to its similar geo-signatures to the Gate zone to the north, which originally catapulted Kodiak into the news with multiple high-grade copper hits. Both Gate and 1516 sit in magnetic lows on the same trend. The 2023 drill results from 1516 are still pending at the date of this writing. Claudia confirmed that MPD South will be the top priority for drilling in 2024, in light of the continuing confirmations that they are getting of the prospectivity of this system. One thing to note is that when Evrim Resources owned the property, they contracted Antofagasta PLC to conduct shallow drilling based on magnetic highs, versus Kodiak's new approach of deep drilling on magnetic lows. Presumably due to a change of focus for the company to royalties, and the fact that they were unable to raise funding, Evrim decided to abandon the work and eventually sold the claims to Kodiak in 2021. Kodiak's fresh approach, with better data and modeling, looks very promising and they will continue to pursue this approach in 2024. Results are also pending for 2023 drilling on the Beyer Zone which presented itself as low-hanging fruit that was efficient to drill and had excellent soil sampling data. 2024 should be an interesting year for Kodiak and I continue to view this company as an excellent longer-term prospect with a current opportunity to accumulate shares at very attractive levels.

Figure 2: MPD South - Courtesy Kodiak Copper Corp