Great news out this week on Aston Bay Holdings (TSX-v: BAY) / (OTCQB: ATBHF). Prominent global metal trading, technical advisory, and financing company Ocean Partners Holdings agreed to fund 80% of the upfront cap-ex on the Storm Copper project.

This strong vote of confidence is important as Aston has a 20% free-carried interest in this valuable asset. The odds of Storm becoming a mine just went up A LOT. Ocean sees what most experts see —> strong demand for Cu, and increasingly uncertain supply. Ocean has vast experience with ore-sorting & direct shipping ore operations.

Ocean Partners’ CEO commented: “We are delighted to be partnering with American West on the Storm Copper Project which is rapidly emerging as a long-life, district-scale copper opportunity.” Notably, the PEA does not (yet) reflect either long-life or district scale. Therein lies the opportunity!

Looking back ~15 years, China started consuming > 50% of the world’s Cu… and still does! This is amazing given that it hosts ~17.5% of the globe’s population.

Chinese leaders are planning additional economic stimulus to counteract the economic impacts of the escalating trade war with the U.S. Economic stimulus is almost always Cu-intensive.

Renewable power + energy storage, AI, data centers, EVs + commercial, industrial, municipal transport + charging infrastructure, the expansion & upgrading of electric grids, 5G telecom, and military weaponry + munitions + transport + logistics + guidance systems + communications —> requires a lot of Cu!

Cu projects that can be in production in years, not decades, in Tier-1 countries, with proximity to large end markets, and low cap-ex, are ideally positioned for a move higher in the Cu price.

In my view, the incentive price to commercialize multi-billion dollar greenfield projects, that are 10-20+ years from commissioning, is meaningfully above today’s level. The world needs all of the technically, environmentally & socially viable mines it can get, even higher-cost ones.

With that in mind, S&P Global’s tracking of Major new Cu discoveries is alarming. From an average of 9.4/yr. in the 1990-2013 period, significant discoveries have collapsed to 1.4/yr. from 2014-2023. This has grave implications for annual supply in the 2030s-2040s.

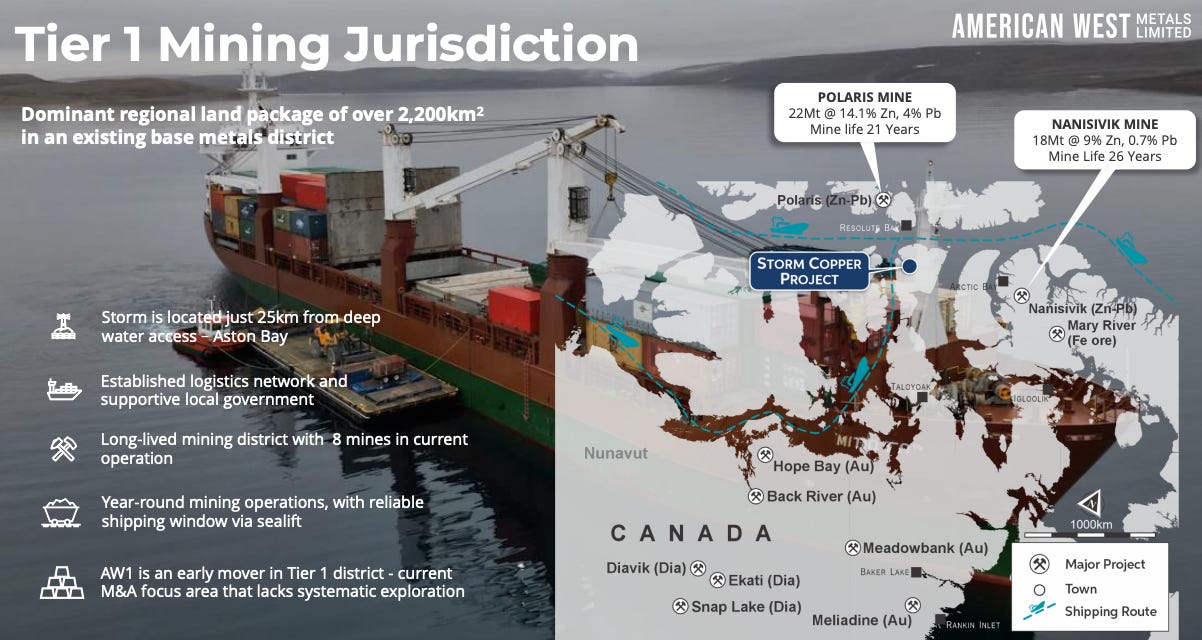

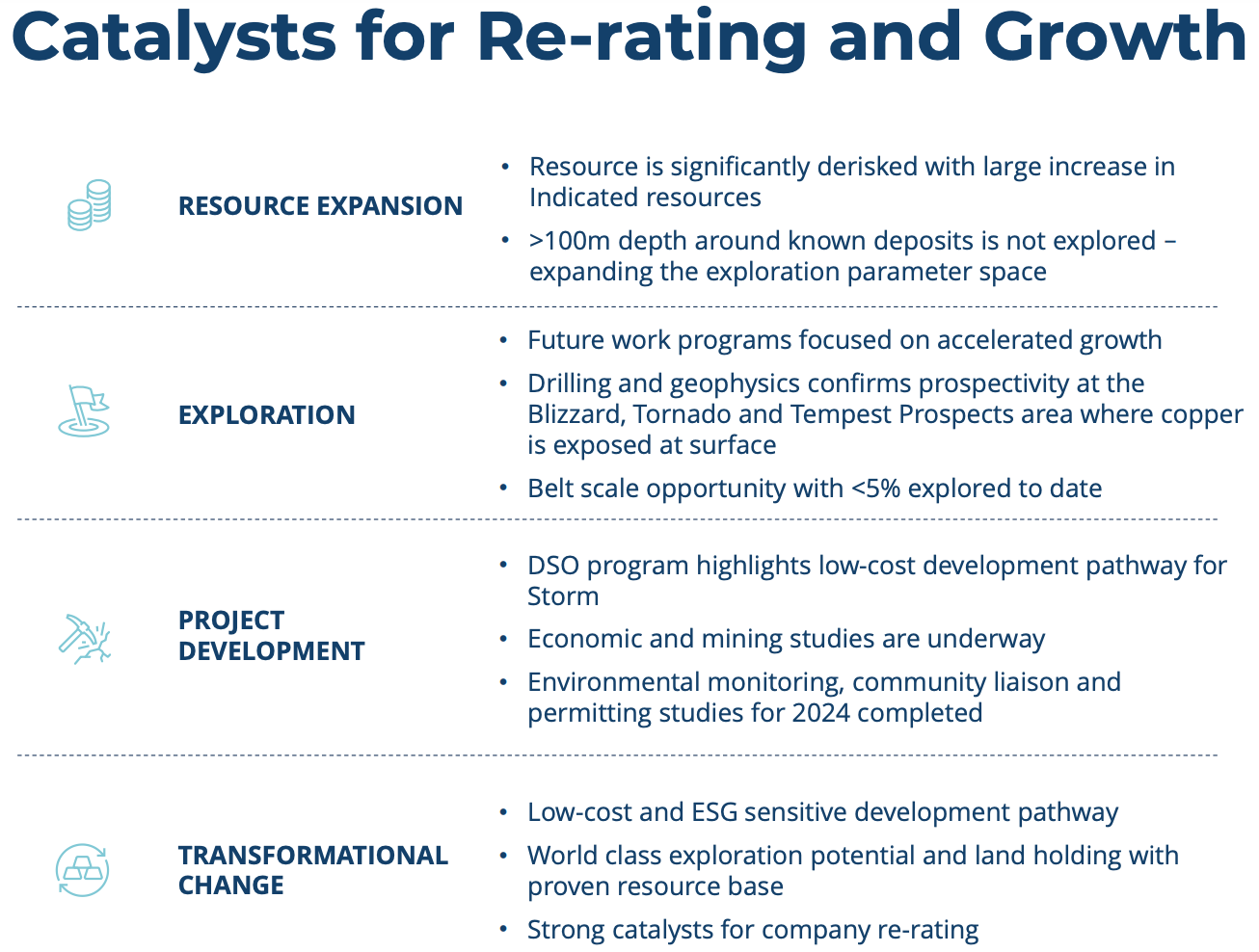

Aston Bay is a tiny company with excellent leverage to Cu (+ some silver). It discovered the exciting high-grade Storm Copper project on Nunavut’s Somerset Island, ~25 km from deepwater shipping on the Norwest Passage, and farmed it out to Australian-listed American West Metals, who now owns 80%.

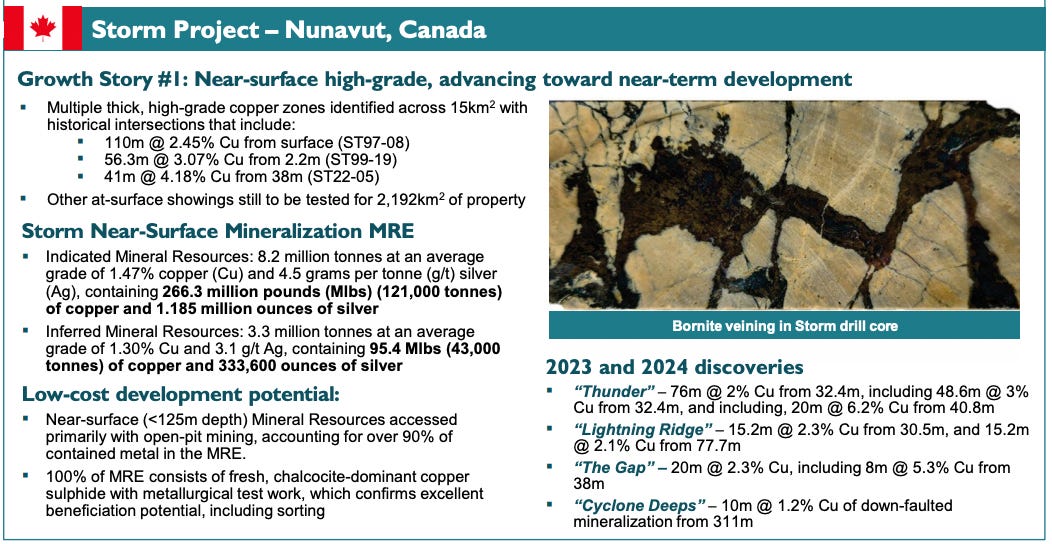

That leaves Aston with a free-carried 20% interest in the [Australian JORC-compliant] PEA-stage project spanning > 2,200 sq. km, upon which Aston recently announced a Canadian NI 43-101 resource estimate for the near-surface mineralization (< 120 meters depth).

It included six deposits within the greater Storm area; Cyclone, Chinook, Corona, Cirrus, Lightning Ridge & Thunder. Drill highlights include 110 m / 2.45% Cu, 56 m / 3.1% Cu, and 48.6 m / 3.0% Cu.

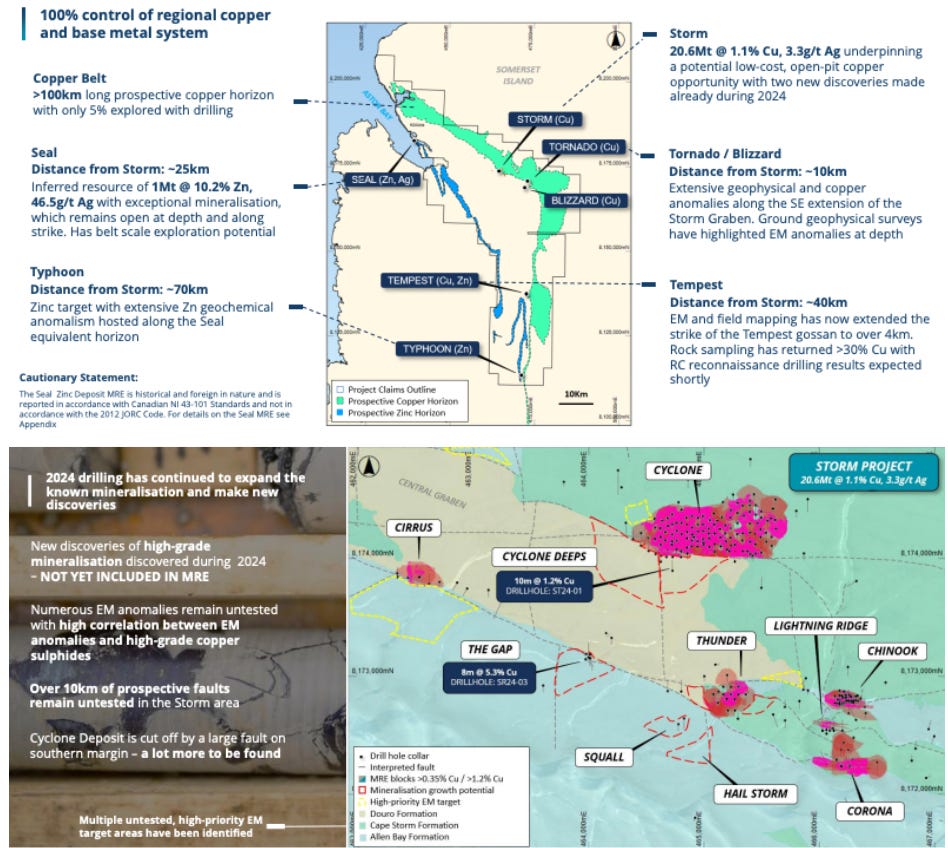

In the images above, note how much blue-sky exploration potential there is. The Project comprises both the Storm & Seal Zinc deposits (best interval at Seal is 22.3 m @ 23.0% Zn, (equiv. to ~6% Cu).

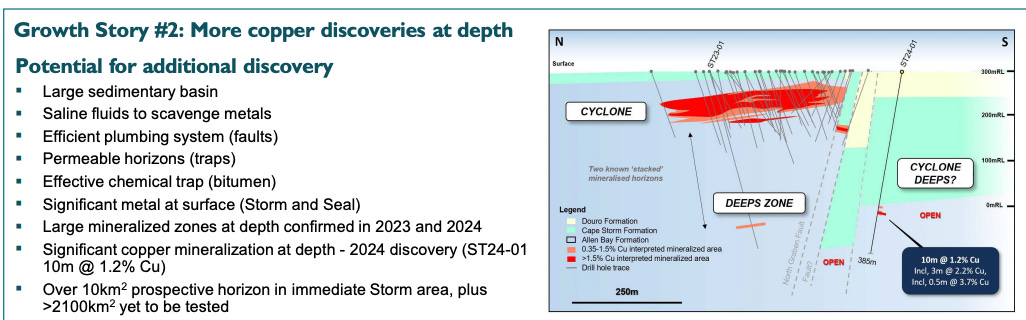

Importantly, there’s strong potential to expand Cu mineralization outside the Storm area. Only 5% of the ~110km long Cu belt has been explored with focused geophysics & drilling. Aston is free-carried through at least two more exploration seasons at Storm. That means the resource size could grow substantially for the full Feasibility Study.

Some complain that Nunavut is too far north. Yet, it’s not too far north for Agnico Eagle, Teck Resources, BHP, MMG Ltd., or B2Gold. Aston owns 20% of the economics of American West’s indicative (JORC) $149M post-tax NPV(8%). An 8% disc. factor is modestly conservative, most gold projects at the PEA stage use a more aggressive 5%.

NOTE: Aston Bay is working on a NI-43-101-compliant PEA, which should look a lot like American West’s.

Aston’s Enterprise Value {market cap + debt - cash} is ~C$10M [$0.055/shr. on 4/9/25]. Compare that to 20% of the $149M NPV = C$42M. I’m not suggesting Aston is worth C$42M today, but C$10M seems too low — a figure that might be warranted if Aston faced major equity dilution for Storm — it doesn’t.

Without relying on a higher Cu price, two more drill seasons (at zero cost to Aston) will deliver a mine life extension and/or an increase in annual production. Therefore, the NPV(8%), or NPV(5%), in next year’s BFS (could be) meaningfully above $149M.

Ocean Partners is covering 80% of the $47.4M in cap-ex — which includes a 25% contingency. That leaves $9.5M to be equity-funded, of which just $1.9M would be Aston’s share. Importantly, readers are reminded that Aston has no funding requirements until after delivery of a BFS (in 2H/26 at the earliest).

As American West/Ocean Partners invest in Storm this year & next. the cap-ex figure will decline. CEO Thomas Ullrich points out that the Company’s 20% share of a royalty signed last year by American West should bring in an additional $1.5M —> of which $0.7M is expected this month. That’s on top of ~$1M on the balance sheet.

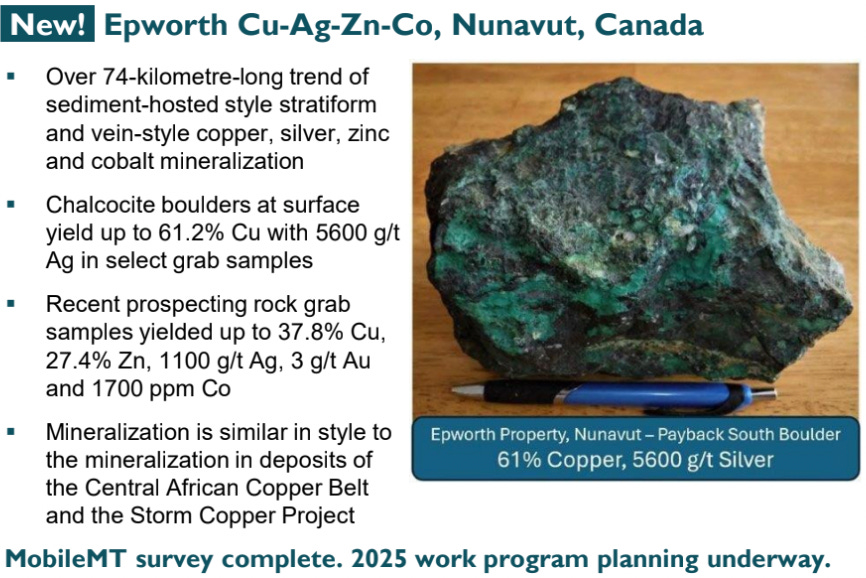

The more I think about Aston’s earn-in opportunity for up to 80% of the promising Epworth property, also in Nunavut, the more I believe it too could be worth a multiple of Aston’s enterprise value.

Of course, that statement is subject to upcoming drilling, following up on samples from chalcocite boulders yielding up to 61.2% Cu + 5,600 g/t Ag. If Epworth becomes Storm Copper 2.0, and management farms out half of its 80% option to get free-carried on 40% for several years — Epworth could be quite valuable.

Importantly, when management negotiated the Epworth transaction in 4Q/23 — 1Q/24, Cu averaged $3.80/lb. Today it’s +16% higher. There are no annual work commitments, just a requirement to invest a total of C$3M over four years.

After further demonstrating the likelihood of a low-cost, high-margin operation at Storm with strong growth potential, a key objective will be to prove Aston can retain its 20% stake, + 20%-40% of Epworth, without excessive equity dilution.

Strategic partners, smelters, royalty/streaming groups & debt providers can help Aston explore/develop Epworth, potentially making its stake worth C$10M’s of millions.

Imagine if American West delivers line-of-site to production by 2028… That would be great news for shareholders, and a meaningful de-risking event for Epworth, allowing management to replicate Storm’s logistics & funding strategies.

Bottom line? Although highly speculative, Aston is free-carried on a 20% interest in Storm Copper, has a low cash burn rate, and is earning up to 80% of Epworth under flexible terms. Its EV of C$10M is low, and the Cu price is rising, making Aston Bay a very compelling risk-adjusted proposition.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Aston Bay Holdings, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Aston Bay are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Aston Bay was an advertiser on [ER] and Peter Epstein owned shares in the company acquired in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.