The EU and US have struck a deal just a few days before the August 1 deadline, narrowly averting a trade war between the two allies who together account for nearly a third of global trade. The agreement — hailed as “the biggest trade deal ever” — feels to some within the 27-nation bloc more like economic appeasement than a victory. Is avoiding disaster really the same as securing a win?

The deal centrepiece is a 15% baseline tariff on EU exports to the U.S., with the exception of steel, which remains subject to a 50% levy. Car imports, currently taxed at 27.5%, will be sold at the new 15% rate.

The EU has also committed to purchase $750 billion in energy from the US over three years. To sweeten the optics of the agreement, the bloc has aggregated all known investment commitments and claimed it will invest $600 billion into the U.S. economy.

Altogether, the tariffs will affect 70% of EU exports worth €380 billion annually. In return, U.S. exports to the EU including cars, currently at 10%, will become duty-free. Trump retains the authority to increase tariffs further if European countries fail to meet their investment commitments.

While the deal technically avoids a full-blown trade war, investors quickly recognized the agreed terms still represent a sharp rise in tariffs — enough to pressure EU exporters and squeeze profit margins across key industries.

The 15% tariff rate applies broadly, including sectors that previously enjoyed minimal duties. That’s bad news for European exporters already grappling with weak demand, persistent inflation, and sluggish economic data.

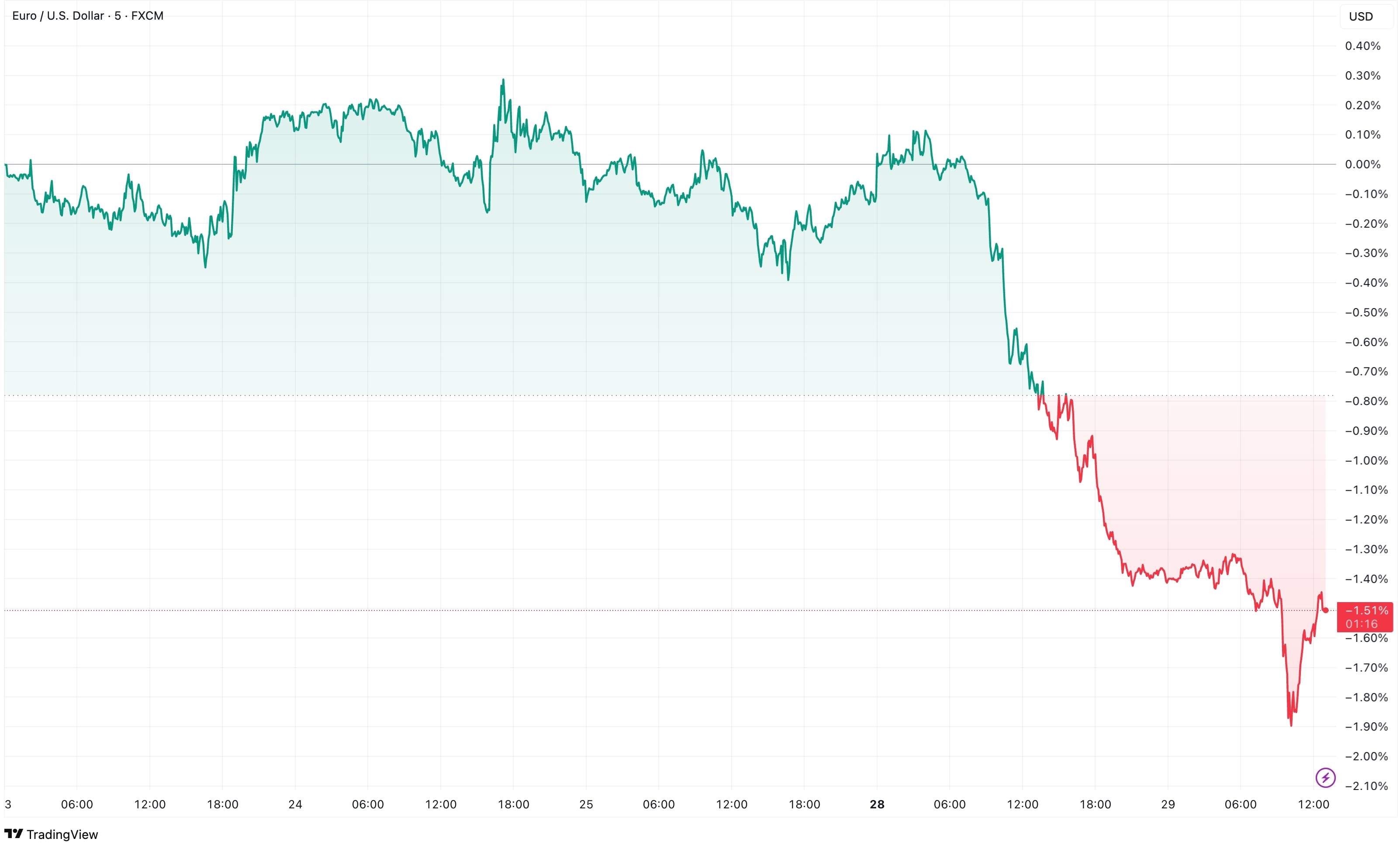

The EUR/USD pair sank 1.3% on Monday — its worst session since May — erasing last week’s gains and pulling away from its four-year high. The selling continued early Tuesday, with the euro dipping into the $1.1550 range.

Beyond economics, the selloff reflects a loss of confidence in the EU’s negotiating strength. Markets now fear that internal political discord could spill over into policymaking, growth, and investor sentiment.

Strong criticism from core EU members — Germany and France — has intensified concerns that the Eurozone’s political cohesion and economic stability are fraying. Forex traders were quick to price in those fears. The frustration stems from the perception that the bloc gave in to U.S. pressure without securing enough in return.

Beyond the deal, traders are also eyeing a trio of market-moving events this week: central bank decisions, inflation prints, and U.S.jobs data.

The Federal Reserve concludes its two-day policy meeting on Wednesday. Chair Jay Powell is widely expected to hold rates steady — again. But markets are already looking past July and placing bets on a rate cut in September.

Donald Trump has publicly pressured the Fed to lower borrowing costs, further escalating political tension. Powell will likely keep a steady tone — but traders will dissect every word of the statement and press conference.

Eurozone inflation data arrives on Friday, with July prices expected to cool to 1.9%, dipping below the European Central Bank’s 2% target for the second time this year.

Also on Friday, the July U.S. nonfarm payrolls report is projected to show 108,000 new jobs, down from June’s 147,000. Slower job growth could strengthen the case for a September rate cut — and apply downward pressure on the dollar. and prompting a pullback in the DXY from its recent strength