Canadian banks are some of the best managed in the world. Relative to the lesser-regulated financial centers like Wall Street and London, Canadian banking has been seen as more responsible yet still with dependable dividend growth and offering long-term value.

It certainly helps that they are some of the largest companies in Canada. Generally, banks have historically received more bailouts than other industries in the US, and the same sense of security is felt in Canada. One caveat to this is that, whilst Canadians often claim their banks didn’t need a bailout in 2008, reports suggest there may have been a $114-billion secret bailout. Still, even in this worst-case scenario, shareholders are often protected by tax-payers' money.

So, how are the ever-reliable Canadian banks doing in today’s turbulent economy, and is it a bad time to be investing in Canadian banks?

How are Canadian banks holding up?

When interest rates rise from 0.25% to 4.5% in under a year, the big banks are the ones to feel its effects directly. In general, banks will pass the rising rates onto the customer, as seen with Royal Bank and TD raising their prime lending rates to 3.7% - 4.7%, along with increasing loan-loss provisions. When borrowers must pay more for their lines of credit, mortgages, and other debt products, demand will drop and customers are at higher risk of default.

That’s the theory, but reality can often be quite different. The number of mortgages in arrears across Canada was 2,426 in November 2022, which is around 0.15% of total mortgages. This figure was actually higher 12 months before (8,531; 0.15%) when inflation and rates were low. So, whilst repayments are costlier along with a higher cost of living, fewer people are behind on repayments… For now.

This can sometimes be cyclical, particularly when relief is handed out. Some analysts believe that Canadian banks will brace for a possible wave of loan defaults later in the year. Across all big six banks, recent reports show a dip in profits and a preparation to handle credit losses.

Are Canadian banks still a good investment?

Many analysts will see the big 6’s move to provide more resources toward upcoming loan defaults as a negative - they expect bad weather. However, the approach sums up the cautious reputation that has gotten them this far, not to mention that a dip in profits isn’t the same as making a loss. The Bank of Canada makes it clear that the big 6 are equipped to withstand sharp declines in GDP (the upcoming recession is expected to be mild), along with spikes in unemployment and sharp falls in house prices.

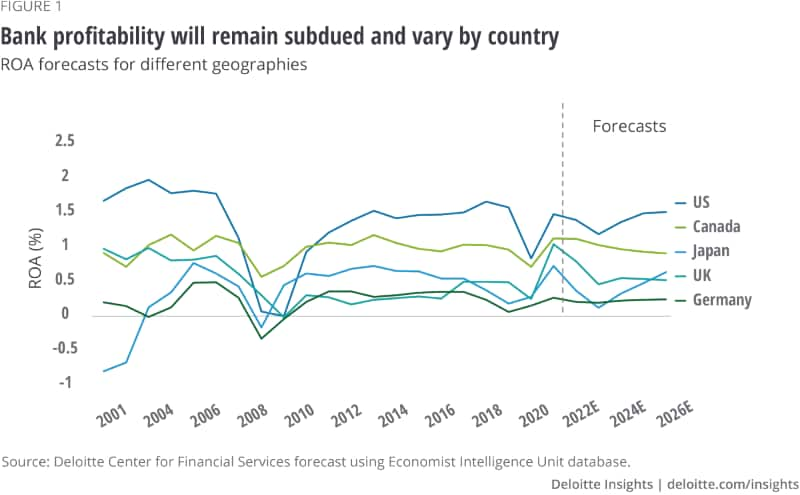

(Please refer to Deloitte Insights' graph of ROA forecasts for different geographies for more information.)

One key factor when looking at whether borrowers can make repayments is their income and job security. Whilst inflation remains high, it is showing signs of tapering off. The economy has recently been described in destitute terms, but Canada’s labor market is relatively healthy with employment up, wage earnings up (though not as high as inflation), and unemployment is down from 2021.

The lack of cheap money that big banks around the world have gotten accustomed to is a definite threat to investors. However, Canadian banks seem better prepared for it than most. One consideration to make is what impact fintech challenger banks will have at a time when the big 6 are under economic pressure.

House prices are another area of risk. Whilst it’s less than many western countries, prices are still expected to fall around 6% in 2023.

Big 6 Q1 2023 summary

Compared to Q1 of 2022, below is a quick summary of how Canadian bank shares and financial reports are performing.

Canadian Imperial Bank of Commerce (CM/TSX) reported a net income of 589 million in Q1/23 was down significantly from last year. Revenue grew to almost $6 billion, however, and outperformed forecasts. Earnings per share dropped from $2.01 in Q1/22 to $0.39 in Q1/23. CM’s share price is -0.29% from a month ago and -22.96% from 12 months ago.

CIBC have their own brokerage named Investors Edge which gives them a diversified income stream.

Bank of Nova Scotia (BNS/TSX) reported for Q1/23, compared to Q1/22, a drop in net income from $2,740 million to $1,772 million, along with a diluted EPS drop from $2.14 to $1.36. When adjusted, these drops are much smaller, but still a $392 million net income fall and $0.30 EPS fall. BNS’s share price is -4.41% in the past month and -23.94% in the past 12 months.

Royal Bank of Canada (RY/TSX) reported a drop in Q1/23 profits as it set aside plenty of loan-loss reserves. However, it still outperformed expectations. EPS dropped from $2.84 a year ago to $2.29 more recently. $532 million was posted for credit loss provisions, almost five times more than Q122. RY’s share price is -2.19% in the past month and about the same in the past 12 months.

National Bank of Canada (NA/TSX) exceeded market expectations by $110 million with a $2.71 billion reported revenue. With 7% YoY growth and an EPS of $2.64 (down just 3%), dividends grew. NA’s stock price is up 2.02% in the past month and up 5.14% in the past 12 months.

Toronto-Dominion Bank (TD/TSX) took a bit of a hammering in the Q1/23 reports. Reported net income was $1,582 million, compared with $3,733 million in Q1/22, though adjusted net income was $4,155 million, compared with $3,833 million. Adjusted diluted EPS were $2.23, compared with $2.08. However, $2.20 was the average analyst’s estimate. TD’s share price is -5.91% in the past month and -11.45% in the past 12 months.

The Bank of Montreal (BMO/TSX) reported a net income of $247 million, compared with $2,933 million in Q1/22. When adjusted, it’s a drop from $2,584 million to $2,272 million. Adjusted EPS fell from $3.89 to $3.22 too, whilst provision for credit loss was $217 million. BMO’s share price is -6.25% from a month ago and -13.43% from 12 months ago.

What lies ahead

The big 6 appear to be taking the right precautions to what is a potential credit and insolvency threat, where customers are seeing living costs rise, repayments rise, and their property prices fall. However, with a relatively healthy labor market, a recession that is expected to be mild at worst, and with profits and loan-loss reserves healthy, there isn’t a catastrophic crisis waiting.

However, Canadian banks do not operate in isolation, so another risk factor to consider is the operations in Wall Street and London. London in particular is at risk, as the economic outlook of the UK is far worse than Canada’s, property prices may decline over 10%, and the country has been more dependent on deregulated cheap money banking.

Clearly, it is only National Bank of Canada’s stock price that is performing well, which may attract momentum investors. But, all 6 Canadian bank stocks are relatively sound for value investors, and research for each should be individually conducted before investing.

This opinion article has been produced exclusively for CEO.ca by Adam Lowerson.

The content is for informational purposes only, and should not be relied upon for, any trading, business, financial, legal, accounting, tax or any other advice.

Copying the article or parts of it is strictly forbidden, unless given permission by the author.

{kind=link}